Permanent life insurance coverage remains a cornerstone of comprehensive financial planning for business owners and their employees. Unlike term policies that expire after a set period, whole life insurance offers guaranteed protection that lasts throughout the policyholder's lifetime, combined with a cash value component that grows over time. For organizations focused on employee financial wellness and long-term stability, understanding this insurance vehicle becomes essential when designing benefits packages and personal wealth strategies. As companies seek to empower their workforce with tools for financial security, permanent insurance options deserve careful consideration.

Understanding the Fundamental Structure

Whole life insurance represents a contract between the policyholder and the insurance company that provides coverage for the insured's entire life, provided premiums are paid as required. The policy combines two primary components: a death benefit that pays out to beneficiaries upon the insured's death, and a cash value account that accumulates over time on a tax-deferred basis.

The premium structure differs significantly from term insurance. Whole life insurance premiums remain level throughout the policy's duration, meaning the amount paid at age 35 stays the same at age 65. This predictability allows for easier long-term budgeting and financial planning.

The Cash Value Component

The cash value element distinguishes whole life insurance from simpler term policies. A portion of each premium payment goes toward building this savings component, which grows at a guaranteed rate set by the insurance company. Many policies also pay dividends, though these are not guaranteed and depend on the insurer's financial performance.

Key characteristics of cash value growth:

- Guaranteed minimum growth rate specified in the policy

- Tax-deferred accumulation without annual tax liability

- Potential dividend payments from participating policies

- Borrowing privileges against the accumulated value

- Surrender value available if the policy is canceled

Business owners can leverage this cash value for various purposes, from funding business expansion to supplementing retirement income. The tax advantages of cash value life insurance make it an attractive component of diversified financial strategies.

Strategic Applications for Business Owners

For entrepreneurs and executives, whole life insurance serves purposes beyond basic protection. The permanent nature and cash value features create opportunities for sophisticated financial planning that align with business objectives.

Business Continuity Planning

Organizations often use permanent insurance as part of buy-sell agreements. When business partners hold policies on each other, the death benefit provides immediate funding to purchase the deceased partner's share from their estate. This arrangement ensures smooth ownership transitions without forcing the sale of business assets or creating financial strain on surviving partners.

Buy-sell agreement benefits:

- Guaranteed funding source at death

- Fixed premium costs throughout the agreement

- Cash value builds as a potential retirement asset

- Tax-free death benefit to fund the buyout

- Protects business operations during transitions

Key Person Insurance

Companies depend on specific individuals whose loss would create significant financial disruption. Whole life insurance on key executives protects the organization while building an asset on the company's balance sheet. The business pays premiums, owns the policy, and receives the death benefit if the key person dies.

The accumulated cash value serves as a corporate asset that can be accessed through policy loans for business needs, creating dual benefits of protection and accessible capital reserves.

| Business Application | Primary Benefit | Secondary Advantage |

|---|---|---|

| Buy-Sell Funding | Guaranteed buyout capital | Cash value accumulation |

| Key Person Coverage | Revenue loss protection | Corporate asset building |

| Executive Benefits | Talent retention tool | Deferred compensation vehicle |

| Estate Planning | Liquidity for estate taxes | Wealth transfer mechanism |

Integration with Employee Benefits Strategies

Organizations committed to comprehensive employee wellness recognize that financial health extends beyond traditional retirement plans. Including permanent insurance options within benefits administration frameworks demonstrates a commitment to long-term employee security.

Voluntary Benefits Programs

Many companies offer whole life insurance as a voluntary benefit, allowing employees to purchase coverage through payroll deduction at potentially lower group rates. This approach provides access to permanent protection for employees who might not otherwise pursue individual policies.

Employees value the stability of fixed premiums and the forced savings element. For workers without disciplined savings habits, the cash value accumulation creates an asset that can be accessed during financial emergencies or used to supplement retirement income.

Executive Compensation Packages

High-level talent often receives whole life insurance as part of compensation arrangements. These policies can be structured as split-dollar arrangements, where the employer and employee share premium costs and benefits, or as pure executive benefits where the company pays premiums as additional compensation.

For organizations focused on empowering employees with financial wellness tools, permanent insurance options complement other benefits by addressing long-term security needs.

Comparing Whole Life to Alternative Options

The life insurance market offers various products, each serving different needs and preferences. Understanding how whole life insurance compares to alternatives helps businesses and individuals make informed decisions.

Whole Life Versus Term Insurance

Term insurance provides pure death benefit protection for a specified period, typically 10, 20, or 30 years. Premiums start lower than whole life but increase dramatically if renewed after the initial term. Term policies build no cash value and expire worthless if the insured outlives the coverage period.

Whole life advantages over term:

- Permanent coverage regardless of age or health changes

- Level premiums that never increase

- Cash value accumulation and access

- Guaranteed death benefit that cannot be outlived

- Potential dividend payments from participating policies

Term insurance advantages:

- Significantly lower initial premiums

- Higher coverage amounts for the same budget

- Simplicity without cash value complexity

- Ideal for temporary needs like mortgage protection

Universal Life Variations

Universal life insurance offers permanent coverage with flexible premiums and death benefits. Unlike whole life's fixed structure, universal life allows policyholders to adjust payments and coverage amounts within limits. However, this flexibility creates uncertainty, as insufficient premium payments can cause policy lapses.

Variable universal life adds investment accounts where policyholders direct cash value into various subaccounts similar to mutual funds. This creates growth potential exceeding whole life's guaranteed rates but introduces market risk that can reduce cash values during downturns.

For businesses seeking predictability in financial planning and employee benefits, whole life insurance's guaranteed values and fixed structure often prove more suitable than variable alternatives.

Financial Mechanics and Policy Performance

Understanding how whole life insurance functions financially helps organizations evaluate its role in comprehensive planning. The mathematics underlying these policies involves actuarial science, mortality tables, and investment projections.

Premium Structure and Allocations

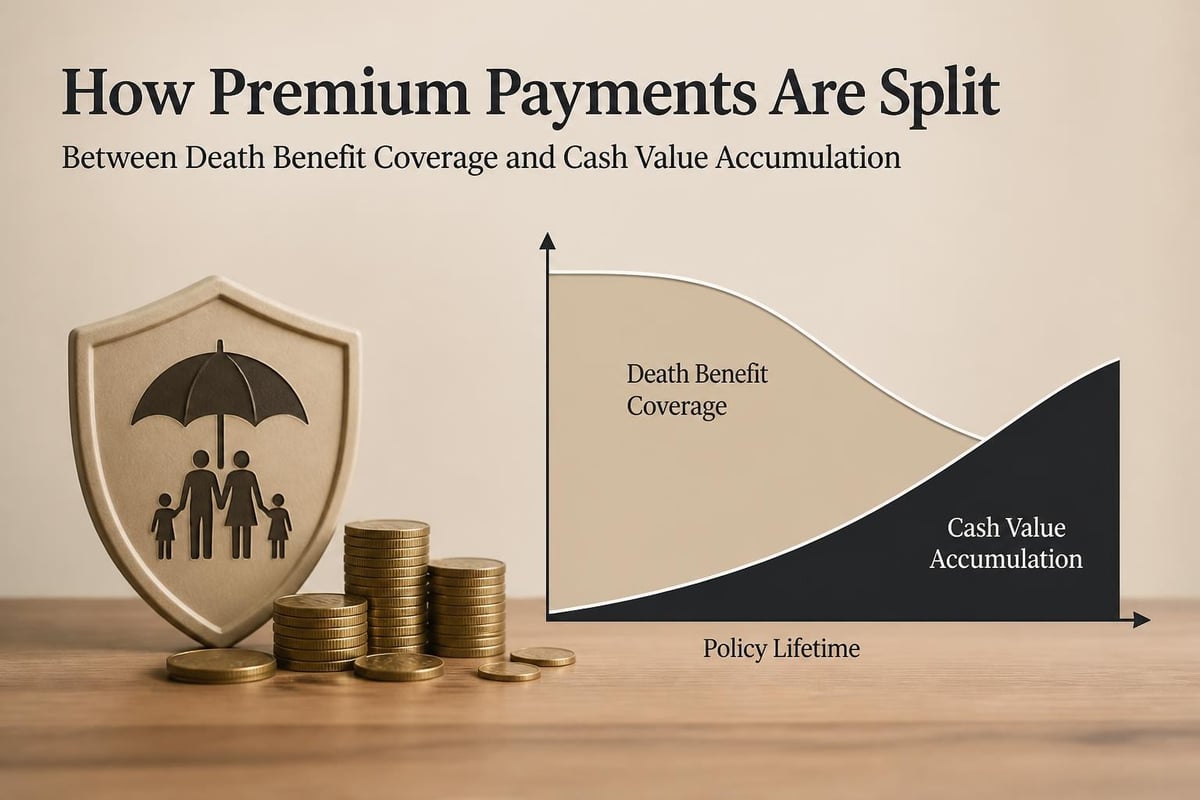

When a policyholder pays premiums, the insurance company allocates funds across several categories. A portion covers the pure cost of insurance based on mortality risk. Administrative expenses and agent commissions consume additional amounts, particularly in early policy years. The remainder flows into the cash value account.

Typical premium allocation in early years:

- Cost of insurance (mortality charges): 30-40%

- Administrative expenses and fees: 20-30%

- Agent commissions: 15-25%

- Cash value contribution: 15-35%

As policies mature, the allocation shifts dramatically. The cost of insurance increases as the insured ages, but cash value contributions grow substantially because commissions and setup costs have been satisfied.

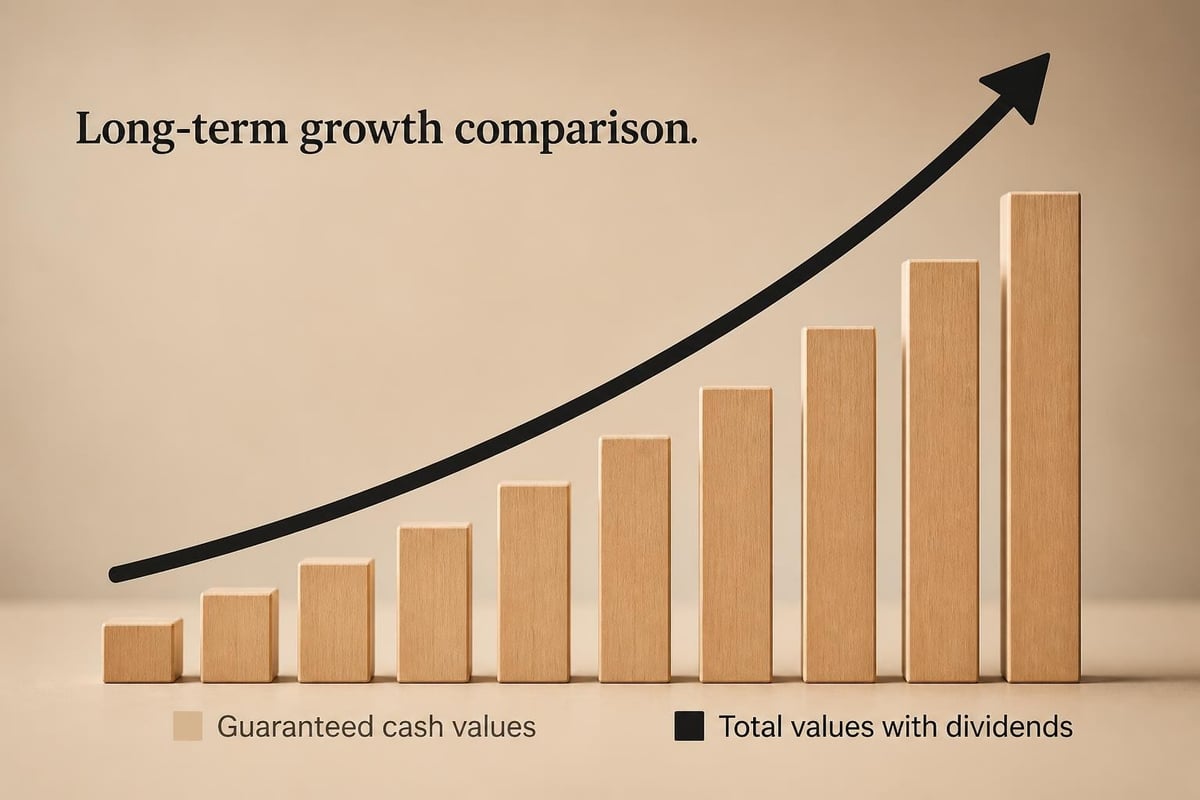

Dividend Payments and Participating Policies

Many whole life insurance policies are "participating," meaning they may pay dividends based on the insurance company's financial performance. These dividends reflect excess investment returns, favorable mortality experience, and efficient operations. Guardian Life and other mutual insurers have paid dividends consistently for decades, though past performance doesn't guarantee future payments.

Dividend usage options:

- Take as cash payment

- Apply toward premium payments

- Purchase paid-up additional insurance

- Accumulate at interest with the insurer

- Repay policy loans

The paid-up additions option increases both death benefit and cash value without requiring evidence of insurability, creating compound growth over time.

| Policy Year | Cumulative Premiums | Guaranteed Cash Value | Potential Total Value* |

|---|---|---|---|

| 5 | $25,000 | $8,500 | $10,200 |

| 10 | $50,000 | $28,000 | $35,600 |

| 20 | $100,000 | $72,000 | $98,400 |

| 30 | $150,000 | $135,000 | $195,000 |

*Assuming non-guaranteed dividends at current rates

Tax Advantages and Considerations

The tax treatment of whole life insurance creates significant advantages for both business and personal financial strategies. Understanding these benefits allows organizations to maximize value when incorporating insurance into compensation and benefits programs.

Tax-Deferred Growth

Cash value accumulates without current income tax liability. Unlike taxable investment accounts where interest, dividends, and capital gains create annual tax obligations, the cash value grows uninterrupted by taxation. This tax deferral advantage compounds over decades, creating substantially greater accumulation than comparable taxable accounts.

Tax-Free Death Benefits

Beneficiaries typically receive death benefit proceeds completely free from federal income tax. For business owners using insurance to fund buy-sell agreements or protect against key person loss, this tax-free benefit provides full funding without tax erosion reducing the available capital.

Estate taxes present separate considerations. While death benefits are income tax-free, they may be included in the insured's taxable estate if the deceased owned the policy. Proper ownership structuring through irrevocable life insurance trusts (ILITs) can remove proceeds from the taxable estate.

Policy Loans and Withdrawals

Policyholders can access cash value through loans without triggering taxable events. The insurance company charges interest on these loans, but policyholders effectively borrow their own money. Outstanding loans reduce the death benefit, and excessive borrowing can cause policy lapse if not managed carefully.

Withdrawals up to the basis (total premiums paid) are also tax-free. Amounts exceeding basis are taxable as ordinary income. For business owners considering retirement income strategies, policy loans provide tax-efficient access to accumulated values.

Risk Factors and Common Misconceptions

While whole life insurance offers substantial benefits, organizations must understand limitations and potential drawbacks when recommending these policies within employee benefits frameworks or using them for business purposes.

Early Year Underperformance

Cash value accumulation starts slowly due to upfront costs. In the first several years, surrender values remain well below cumulative premiums paid. Businesses purchasing policies for key persons or executives should maintain these policies long-term to realize their full value proposition.

Cash value break-even typically occurs:

- Years 7-10 for traditional whole life policies

- Years 5-7 for lower commission or direct-sold policies

- Years 12-15 when comparing to term insurance cost differences

Opportunity Cost Considerations

The premium costs for whole life insurance exceed term insurance by substantial margins. The difference could be invested in other vehicles potentially generating higher returns. This "buy term and invest the difference" argument has merit for disciplined investors with long time horizons.

However, this comparison ignores behavioral factors. Many individuals fail to invest the premium difference consistently, while whole life insurance forces systematic savings. For employee financial wellness programs, the forced savings element provides value beyond pure mathematical optimization.

Inflation and Fixed Benefits

Traditional whole life insurance provides fixed death benefits that don't automatically adjust for inflation. A $500,000 policy purchased in 2026 will still pay $500,000 in 2056, despite inflation potentially halving the purchasing power. Participating policies partially address this through dividend purchases of additional insurance, but inflation protection remains imperfect.

Evaluating Suitability for Different Situations

Not every organization or individual needs whole life insurance. Matching insurance products to specific situations ensures resources are allocated efficiently while meeting protection and savings objectives.

Ideal Candidates for Whole Life Coverage

Business owners with permanent insurance needs and strong cash flow benefit significantly from whole life policies. The guaranteed values, predictable premiums, and tax advantages align well with long-term business planning requirements.

Organizations and individuals who benefit most:

- Business owners funding buy-sell agreements

- High-income professionals maximizing tax-advantaged savings

- Parents seeking guaranteed inheritance for children

- Individuals with estate tax exposure needing liquidity

- Conservative savers preferring guaranteed growth

Companies serving enterprise clients and mid-market organizations often find whole life insurance valuable for executive retention and business continuity planning.

When Alternative Solutions Work Better

Younger professionals with limited budgets and temporary protection needs typically fare better with term insurance. The lower premiums allow higher coverage amounts during peak responsibility years when mortgage debt and dependent children create maximum financial exposure.

Sophisticated investors comfortable with market volatility might prefer maximizing tax-advantaged retirement accounts like 401(k) plans and IRAs before committing to whole life insurance. These vehicles often provide better long-term returns despite lacking the guarantees inherent in whole life policies.

Selecting Carriers and Policy Structures

The financial strength and stability of the insurance company issuing whole life policies matters tremendously. These contracts span decades, and policyholders need confidence that the insurer will fulfill obligations regardless of economic conditions.

Financial Strength Ratings

Independent rating agencies like A.M. Best, Moody's, and Standard & Poor's assess insurance company financial stability. Organizations purchasing policies for business purposes should limit consideration to carriers rated A+ or higher from A.M. Best, or equivalent ratings from other agencies.

Mutual insurance companies, owned by policyholders rather than shareholders, have demonstrated particular stability in the whole life insurance market. Their focus on long-term policyholder value rather than quarterly shareholder returns aligns well with the permanent nature of these contracts.

Policy Design Considerations

Modern whole life insurance offers customization through riders and optional features that enhance basic coverage. Accelerated death benefit riders allow access to proceeds if diagnosed with terminal illness. Waiver of premium provisions continue coverage if the insured becomes disabled and cannot pay premiums.

Common valuable riders:

- Accelerated death benefit for terminal illness

- Waiver of premium for disability

- Guaranteed insurability options for future purchases

- Long-term care benefit riders

- Accidental death benefit provisions

Organizations designing comprehensive employee benefits packages should evaluate which riders provide meaningful value for their workforce demographics and needs.

Implementation Within Organizational Frameworks

For companies committed to employee financial wellness, implementing whole life insurance options requires thoughtful integration with existing benefits programs and clear communication about product features and limitations.

Education and Enrollment Support

Employees often struggle to understand permanent insurance differences from term coverage. Educational programs explaining premium structures, cash value growth, and appropriate use cases help employees make informed decisions aligned with their personal financial situations.

Providing access to licensed advisors who can evaluate individual circumstances ensures employees select appropriate coverage amounts and product types. This personalized guidance increases enrollment satisfaction and reduces post-purchase regret.

Monitoring and Ongoing Support

Whole life insurance policies require periodic review to ensure they continue meeting objectives. Annual statements show cash value growth, dividend payments, and death benefit levels. Organizations offering these benefits should facilitate regular reviews and provide resources for employees managing their policies effectively.

For business-owned policies covering key personnel or funding buy-sell agreements, annual reviews ensure adequate coverage amounts as business values change and confirm premium payments remain current.

Whole life insurance represents a sophisticated financial tool that combines permanent protection with forced savings and tax advantages, making it valuable for business continuity planning and comprehensive employee benefits programs. When properly structured and maintained, these policies provide guaranteed outcomes that support long-term financial security for organizations and their workforce. Nero and Associates, Inc. helps organizations design comprehensive benefits strategies that empower employees with financial wellness tools while optimizing operational efficiency and controlling costs. Our consultative approach ensures your employee benefits package aligns with both workforce needs and organizational objectives, creating sustainable value for everyone involved.