Understanding and optimizing collection rates has become a critical imperative for organizations navigating the complex financial landscape of 2026. These metrics directly impact cash flow, operational efficiency, and overall financial health, making them essential KPIs for businesses across industries. Whether you're managing accounts receivable internally or working with external partners, the ability to measure, benchmark, and improve your collection performance can mean the difference between sustainable growth and financial stagnation. For professional services firms and consulting organizations, maintaining healthy collection rates ensures resources remain available for innovation, talent development, and client service excellence.

Defining Collection Rates and Key Metrics

Collection rates represent the percentage of outstanding receivables successfully recovered within a specific timeframe. This metric serves as a fundamental indicator of financial operational efficiency and customer payment behavior.

The most common calculation divides total collections by total receivables, multiplied by 100 to express the result as a percentage. However, sophisticated organizations track multiple variations of this metric to gain deeper insights into their revenue cycle performance.

Primary Collection Rate Metrics Include:

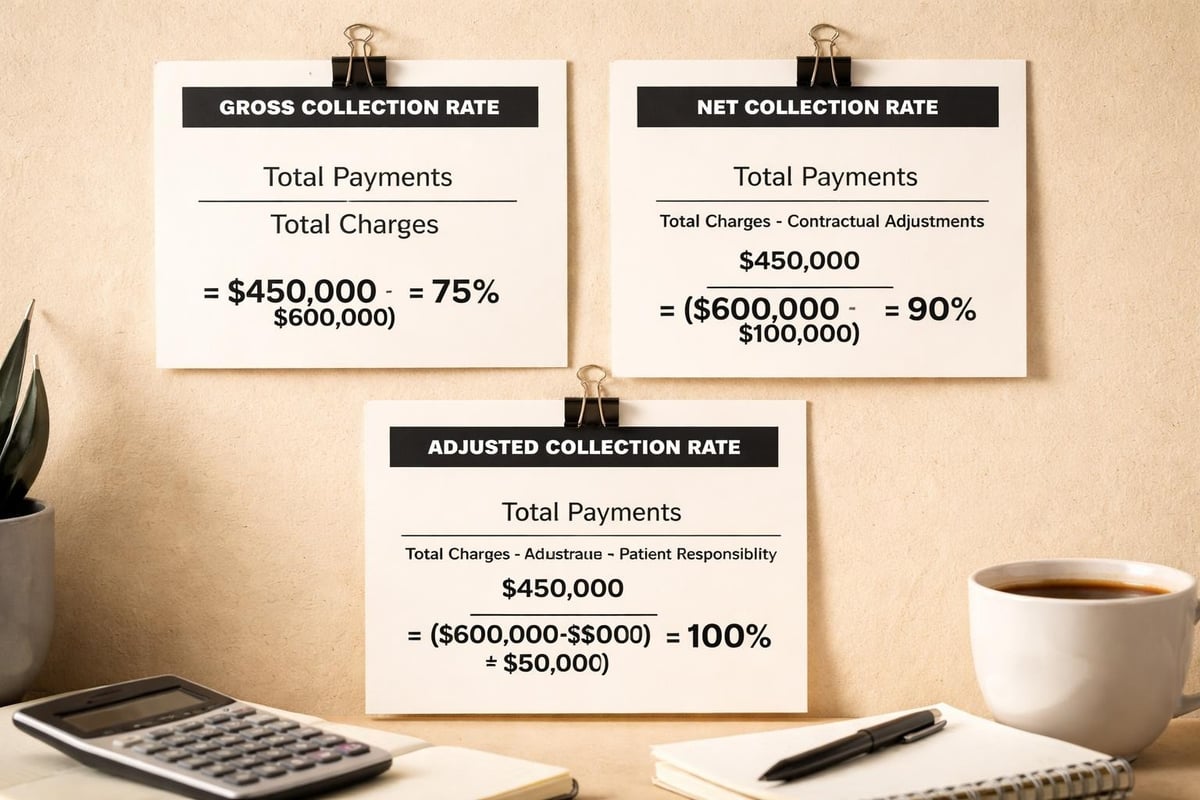

- Gross Collection Rate: Total payments received divided by total charges

- Net Collection Rate: Total payments divided by total collectible amount (after contractual adjustments)

- Adjusted Collection Rate: Payments divided by net revenue (accounting for all adjustments)

- Time-Based Collection Rate: Recovery percentage within specific aging buckets (30, 60, 90 days)

According to recent industry statistics, the average recovery rate for third-party debt buyers reached 18.3% in 2022, representing a decline from 20.1% in 2020 due to economic uncertainty. These benchmarks highlight the importance of proactive internal collection strategies before accounts reach external agencies.

Industry Benchmarks and Performance Standards

Collection rates vary significantly across industries, debt types, and organizational structures. Understanding where your performance stands relative to industry standards provides crucial context for improvement initiatives.

| Industry Sector | Average Collection Rate | Optimal Timeframe |

|---|---|---|

| Property Management | 20%-40% | 60-90 days |

| Utility Services | 20%-35% | 45-60 days |

| Commercial B2B | 70%-85% | Under 90 days |

| Healthcare | 15%-25% | 90-120 days |

| Professional Services | 65%-80% | 30-60 days |

Professional services firms typically experience higher collection rates than other sectors, primarily due to established client relationships and contract-based payment terms. However, maintaining these rates requires consistent process discipline and proactive account management.

Research indicates that commercial B2B recovery rates can reach 70-85% when debts are referred to professional collection agencies within 90 days of default. This data underscores the critical importance of timely intervention in the collection process.

Factors Influencing Collection Performance

Multiple variables affect an organization's ability to maintain strong collection rates. Understanding these factors enables targeted interventions that address root causes rather than symptoms.

Timing and Account Age

The age of receivables represents the single most significant predictor of collection success. Fresh accounts maintain substantially higher recovery probabilities than aged debts.

Accounts less than 30 days past due typically yield collection rates exceeding 80%, while accounts aged beyond 180 days may drop below 30%. This deterioration accelerates as time passes, with each month reducing recovery likelihood by approximately 5-10%.

Organizations tracking their average collection period gain valuable insights into payment patterns and can identify problematic trends before they impact cash flow significantly. This metric calculates how long clients typically take to pay invoices, providing a baseline for performance improvement.

Critical Timing Considerations:

- First contact within 7 days of invoice due date

- Escalation protocols for accounts reaching 45 days past due

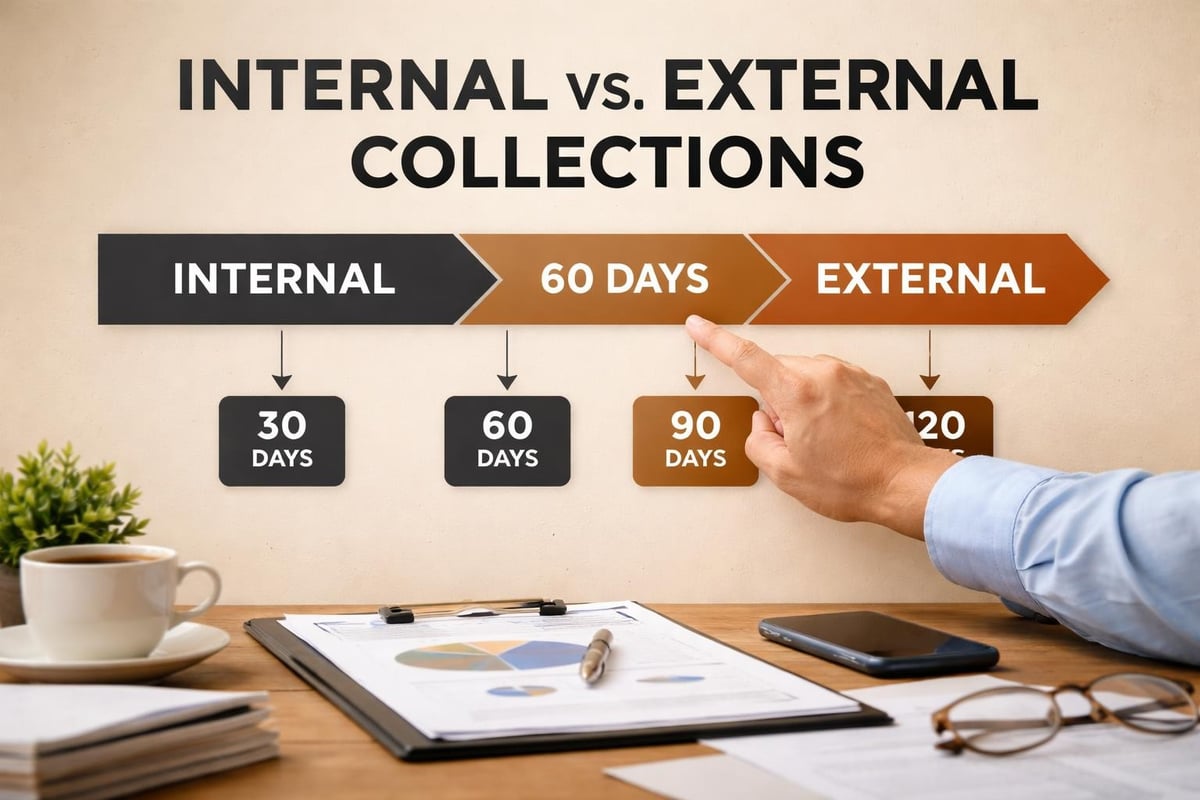

- Internal collection efforts focused on 30-90 day window

- External agency referral decisions at 90-120 day mark

Customer Communication and Relationship Quality

The strength of client relationships directly correlates with payment behavior and collection rates. Organizations maintaining regular communication, transparency, and customer service excellence typically experience fewer collection challenges.

Proactive communication strategies include payment reminders before due dates, immediate acknowledgment of payments received, and courteous follow-up on overdue accounts. These practices maintain positive relationships while reinforcing payment expectations.

For consulting firms and professional services providers, the relationship dynamic adds complexity to collection efforts. Balancing firm collection practices with ongoing client relationships requires diplomatic skill and clear policies understood by both parties from engagement inception.

Strategic Approaches to Improving Collection Rates

Optimizing collection performance requires systematic approaches that address people, processes, and technology components of the revenue cycle.

Process Optimization and Automation

Modern organizations leverage automation and integration technologies to streamline collection processes, reduce manual effort, and accelerate payment cycles. These solutions can eliminate thousands of hours traditionally spent on repetitive tasks while improving consistency and reducing errors.

Automated systems can send payment reminders on predetermined schedules, escalate overdue accounts based on aging criteria, and flag high-risk accounts for immediate attention. Integration between invoicing systems, customer relationship management platforms, and payment processors creates seamless workflows that reduce friction in the payment process.

Implementing accounts receivable collections best practices ensures systematic approaches to managing outstanding balances, from invoice delivery through final payment reconciliation.

Automation Opportunities:

- Automated invoice delivery via email or customer portals

- Scheduled payment reminders at 7, 14, and 21 days before due date

- Escalation workflows triggering at predetermined aging intervals

- Real-time payment posting and account reconciliation

- Dashboard reporting for collection performance tracking

Credit Policy and Terms Management

Prevention proves more effective than cure in accounts receivable management. Establishing clear credit policies, conducting appropriate credit checks, and setting realistic payment terms based on customer risk profiles reduces collection challenges before they arise.

Organizations should regularly review credit policies to ensure alignment with current market conditions, customer payment behaviors, and business objectives. Terms that are too lenient increase bad debt risk, while overly restrictive policies may hinder competitive positioning.

| Credit Risk Level | Payment Terms | Deposit Requirement | Credit Limit |

|---|---|---|---|

| Low Risk | Net 60 | None | $50,000+ |

| Medium Risk | Net 30 | None | $25,000 |

| High Risk | Net 15 | 25-50% | $10,000 |

| New Customer | COD/Prepay | 50-100% | $5,000 |

These tiered approaches balance business development objectives with financial risk management, enabling organizations to serve diverse customer segments while protecting collection rates.

External Collection Resources and Cost Considerations

When internal collection efforts prove insufficient, external collection agencies provide specialized expertise and resources to recover outstanding debts. Understanding the cost structures and selection criteria for these partners ensures optimal outcomes.

Agency Fee Structures and Economics

Collection agencies typically operate on contingency fee models, earning compensation only when they successfully recover funds. Agency compensation structures typically range from 15-35% of recovered amounts, creating alignment between agency incentives and client outcomes.

Commercial debt collection rates commonly follow tiered structures, with 25% on the first $5,000 collected and 20% on remaining balances for US debt collection. However, multiple factors affect costs, including account age, debt size, debtor location, and collection complexity.

Organizations should evaluate agency partners based on:

- Industry specialization and expertise

- Recovery rate track records in relevant debt categories

- Compliance and regulatory adherence

- Technology integration capabilities

- Reporting transparency and communication protocols

Balancing Internal and External Collection Efforts

Optimal collection strategies combine internal processes for recent receivables with external expertise for aged or complex accounts. This hybrid approach maximizes recovery while minimizing costs and maintaining customer relationships where possible.

Internal teams focus on accounts under 90 days past due, leveraging existing customer relationships and organizational knowledge. External agencies handle aged accounts where internal efforts have been exhausted, bringing specialized negotiation skills and legal expertise to challenging situations.

Technology and Data-Driven Collection Management

Advanced analytics and artificial intelligence are transforming collection operations in 2026, enabling predictive modeling, personalized outreach strategies, and automated decision-making that improves collection rates while reducing operational costs.

Predictive Analytics and Risk Scoring

Machine learning algorithms analyze historical payment data, customer characteristics, and external factors to predict payment probability and optimal collection strategies for individual accounts. These insights enable prioritization of collection efforts toward accounts with highest recovery potential and greatest financial impact.

Risk scoring models assign probability ratings to outstanding receivables, helping collection teams allocate resources efficiently. High-risk accounts receive immediate attention with intensive collection efforts, while low-risk accounts may require only standard reminder processes.

Data Points for Predictive Modeling:

- Historical payment patterns and timeliness

- Invoice size and frequency

- Customer industry and economic conditions

- Credit score and financial stability indicators

- Communication response rates and preferences

- Previous dispute history and resolution outcomes

Performance Monitoring and Continuous Improvement

Sophisticated organizations establish comprehensive dashboards tracking collection rates across multiple dimensions, including time periods, customer segments, collection staff, and debt ages. This granular visibility enables rapid identification of performance issues and opportunities for improvement.

Regular analysis of collection metrics should examine trends over time, compare performance against benchmarks, and identify outliers requiring investigation. Monthly or quarterly reviews ensure accountability and drive continuous refinement of collection processes.

Key performance indicators extend beyond simple collection rates to include days sales outstanding (DSO), aging bucket distribution, collector productivity metrics, and customer satisfaction scores. This holistic view ensures collection optimization doesn't compromise other business objectives.

Organizational Culture and Collection Effectiveness

The human element remains central to collection success despite technological advances. Organizations with strong collection rates cultivate cultures that value financial discipline, customer service excellence, and cross-functional collaboration.

Training and Skill Development

Collection effectiveness depends heavily on staff capabilities in communication, negotiation, conflict resolution, and financial analysis. Investing in comprehensive training programs develops these competencies while ensuring compliance with regulatory requirements and organizational policies.

Effective collectors balance assertiveness with empathy, maintain professionalism under difficult circumstances, and demonstrate creative problem-solving when standard approaches prove insufficient. These skills require ongoing development through formal training, mentoring, and performance feedback.

Organizations serving diverse industries, such as consulting companies in Philadelphia working across multiple sectors, benefit from collectors who understand industry-specific payment norms and challenges affecting different client segments.

Cross-Functional Alignment

Collection success requires coordination across sales, customer service, finance, and operations teams. Misalignment between departments creates confusion, inconsistent customer experiences, and reduced collection rates.

Sales teams must clearly communicate payment terms during the sales process and avoid commitments that undermine collection policies. Customer service representatives need visibility into account status to address payment inquiries effectively. Operations teams should understand how delivery issues or service quality problems impact payment willingness.

Regular cross-functional meetings ensure shared understanding of collection priorities, customer situations, and process improvements. This collaboration prevents silos that create gaps in the collection process.

Legal and Regulatory Compliance Considerations

Collection activities operate within complex regulatory frameworks designed to protect consumers and ensure fair treatment. Organizations must maintain rigorous compliance to avoid legal liability, reputational damage, and financial penalties.

Regulatory Requirements and Best Practices

The Fair Debt Collection Practices Act (FDCPA) and state-level regulations establish boundaries for collection communications, prohibited practices, and consumer rights. While primarily applicable to third-party collectors, these principles inform ethical collection practices for all organizations.

Compliance requirements include accurate record-keeping, validation of debt amounts, respect for communication preferences, and cessation of contact when legally required. Violations carry significant penalties and can trigger costly litigation.

Organizations should implement compliance monitoring programs, regular staff training, and documented procedures ensuring consistent adherence to legal requirements. Technology solutions can enforce compliance by preventing communications outside permitted hours, tracking consent documentation, and maintaining audit trails.

Documentation and Dispute Management

Comprehensive documentation protects organizations during disputes and provides evidence supporting collection efforts. Every communication, payment promise, and account modification should be recorded with dates, participants, and outcomes clearly documented.

When customers dispute charges, prompt investigation and transparent communication prevent escalation while maintaining collection rates. Legitimate disputes should be resolved quickly and fairly, while unfounded disputes require firm responses supported by documentation.

Clear dispute resolution processes balance customer satisfaction with financial protection, ensuring organizations neither write off valid receivables nor damage relationships over misunderstandings.

Optimizing collection rates requires strategic focus across technology, processes, people, and partnerships, with disciplined execution creating sustainable improvements in cash flow and financial performance. Organizations that invest in comprehensive collection strategies position themselves for stronger financial health and competitive advantage. Nero and Associates, Inc. helps businesses transform their revenue cycle operations through automation, process optimization, and data-driven insights that eliminate manual inefficiencies while improving collection outcomes. Our performance-based approach ensures measurable results that directly impact your bottom line and operational efficiency.