Organizations investing in complex assets face a critical accounting challenge: how to accurately reflect the value and useful life of equipment with multiple components that wear out at different rates. Component depreciation addresses this challenge by requiring businesses to separately depreciate each significant part of property, plant, and equipment when those parts have materially different useful lives or consumption patterns. This approach transforms how companies manage their capital investments, providing more accurate financial reporting and enabling smarter decision-making about asset maintenance, replacement, and capital allocation.

Understanding Component Depreciation Fundamentals

Component depreciation represents a sophisticated accounting methodology that recognizes the economic reality of complex assets. Rather than treating an entire piece of equipment as a single depreciable unit, component depreciation requires identifying and separately depreciating each significant part with a distinct useful life or benefit pattern.

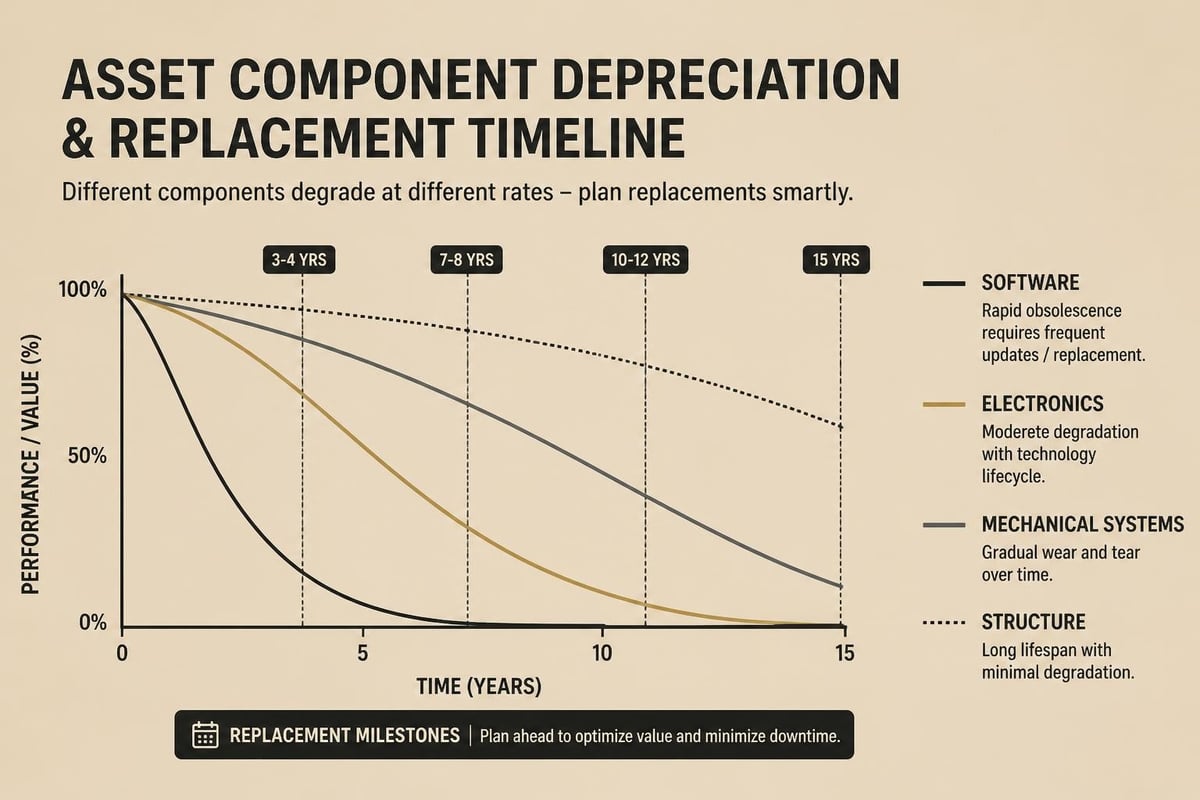

This approach acknowledges that a commercial building's roof, HVAC system, elevator, and structural components all deteriorate at different rates and require replacement at different intervals. The same principle applies to manufacturing equipment, medical devices, and technology infrastructure where individual components have varying lifespans.

The Accounting Framework Behind Componentization

The component depreciation method emerged primarily from International Financial Reporting Standards (IFRS), specifically IAS 16, which mandates this approach for property, plant, and equipment. Under this framework, organizations must allocate the initial cost of an asset to its significant components and depreciate each separately based on its individual useful life.

Key requirements include:

- Identification of significant components at acquisition or construction

- Allocation of total asset cost to individual components

- Determination of separate useful lives for each component

- Application of appropriate depreciation methods per component

- Regular review and adjustment of component classifications

While U.S. GAAP does not explicitly require component depreciation, the differences between IFRS and US GAAP approaches create important considerations for multinational organizations. Many companies adopt componentization voluntarily for improved asset management even when not strictly required by their reporting standards.

Practical Application in Business Operations

Organizations implementing component depreciation must develop systematic processes for asset componentization. Asset componentization involves recognizing distinct, significant parts of complex assets as separate items in the asset register, each with its own cost allocation, useful life determination, and depreciation schedule.

The implementation process requires cross-functional collaboration between accounting, operations, and maintenance teams. Finance professionals need technical input to accurately estimate component useful lives, while operational teams benefit from the enhanced visibility into asset replacement timing that component depreciation provides.

Identifying Significant Components

Determining which parts qualify as significant components requires professional judgment based on materiality and economic substance. A component is typically considered significant when its cost represents a substantial portion of the total asset value and it has a useful life materially different from other components.

Common examples of componentization:

| Asset Type | Typical Components | Varying Useful Lives |

|---|---|---|

| Commercial Building | Structure, roof, HVAC, elevator, parking lot | 40, 20, 15, 25, 10 years |

| Manufacturing Equipment | Frame, motor, electronics, safety systems | 25, 10, 7, 12 years |

| Medical Imaging Device | Housing, imaging sensor, computer system, software | 15, 8, 5, 3 years |

| Fleet Vehicles | Chassis, engine, transmission, electronics | 10, 7, 8, 5 years |

For healthcare organizations working to optimize revenue cycle management, component depreciation provides more accurate cost allocation for expensive medical equipment, enabling better pricing decisions and reimbursement strategies.

Component Depreciation Methodology and Calculation

The mathematical approach to component depreciation builds upon traditional depreciation methods while adding layers of complexity. The component depreciation process involves separating a large asset into multiple components, allocating the total acquisition cost proportionally, and applying individual depreciation calculations.

Step-by-Step Implementation Process

- Acquire and record the asset at total cost including all capitalized expenses

- Identify significant components based on materiality and distinct useful lives

- Allocate total cost to components using fair value proportions or engineering estimates

- Determine useful life for each component based on technical specifications and usage patterns

- Select depreciation method (straight-line, declining balance, units of production) per component

- Calculate periodic depreciation for each component separately

- Record depreciation expense aggregating all component amounts

- Monitor and review components for impairment or useful life changes

When organizations leverage artificial intelligence and automation solutions, they can streamline component tracking and automate depreciation calculations across thousands of asset components, reducing manual processes and improving accuracy.

Practical Calculation Example

Consider a healthcare facility purchasing a diagnostic imaging system for $2,000,000. The componentization analysis identifies:

- Imaging housing and structure: $600,000 (30%) – 15-year life

- Imaging sensor technology: $800,000 (40%) – 8-year life

- Computer and processing system: $400,000 (20%) – 5-year life

- Software and AI algorithms: $200,000 (10%) – 3-year life

Using straight-line depreciation, annual expenses would be:

| Component | Cost | Useful Life | Annual Depreciation |

|---|---|---|---|

| Housing/Structure | $600,000 | 15 years | $40,000 |

| Sensor Technology | $800,000 | 8 years | $100,000 |

| Computer System | $400,000 | 5 years | $80,000 |

| Software/AI | $200,000 | 3 years | $66,667 |

| Total | $2,000,000 | Varies | $286,667 |

Without component depreciation, treating this as a single asset with a 15-year life would yield only $133,333 annual depreciation, significantly understating costs in early years and overstating them later.

Strategic Benefits for Organizations

Component depreciation delivers significant advantages beyond technical accounting compliance. Organizations adopting this methodology gain enhanced financial transparency, improved capital planning capabilities, and more accurate performance metrics.

The strategic value becomes particularly evident when planning maintenance budgets and capital replacement schedules. By tracking component-level depreciation, organizations can anticipate replacement needs years in advance and allocate resources more efficiently.

Financial Reporting Accuracy

Component depreciation provides a more faithful representation of asset consumption patterns. The method aligns depreciation expense with the actual economic benefits received from assets over time, improving the matching principle in accrual accounting.

This enhanced accuracy supports better decision-making across multiple organizational functions:

- Capital budgeting: More precise long-term investment planning based on realistic replacement timelines

- Pricing strategies: Accurate cost allocation supporting pricing decisions and profitability analysis

- Performance measurement: True operational efficiency metrics unaffected by distorted depreciation

- Tax planning: Optimized tax positions through appropriate component useful life determinations

- Asset management: Data-driven maintenance and replacement decisions

For non-profit organizations managing donor funds, component depreciation demonstrates fiscal responsibility through accurate asset cost tracking and transparent financial reporting.

Operational Efficiency Gains

Beyond accounting benefits, component depreciation creates operational value by integrating financial tracking with physical asset management. Maintenance teams gain clear visibility into component lifecycles, enabling proactive replacement planning rather than reactive emergency repairs.

Organizations report these operational improvements:

- Reduced unplanned downtime through predictive component replacement

- Lower total cost of ownership via optimized maintenance timing

- Enhanced warranty management by tracking component-specific coverage periods

- Improved vendor negotiations using detailed component cost data

- Better insurance coverage through accurate asset valuation

Regulatory and Compliance Considerations

Component depreciation intersects with various regulatory frameworks depending on organizational structure and reporting requirements. Understanding these compliance dimensions ensures proper implementation while avoiding costly errors.

Federal regulations provide guidance on acceptable depreciation methods for tax purposes, though tax depreciation may differ from book depreciation under component approaches. Organizations must maintain separate tracking systems when book and tax treatments diverge.

IFRS vs. GAAP Requirements

The mandatory nature of component depreciation varies significantly between accounting standards. IFRS explicitly requires componentization under IAS 16, while U.S. GAAP permits but does not mandate this approach for most organizations.

| Aspect | IFRS (IAS 16) | U.S. GAAP |

|---|---|---|

| Component requirement | Mandatory for significant parts | Optional, permitted but not required |

| Materiality threshold | Professional judgment | Professional judgment |

| Revaluation allowed | Yes, with restrictions | No, cost model only |

| Componentization detail | Detailed guidance provided | Limited specific guidance |

Healthcare organizations processing AI-enhanced claims must ensure their component depreciation approaches align with regulatory cost reporting requirements, particularly for Medicare cost reports and other reimbursement calculations.

Implementation Challenges and Solutions

Organizations transitioning to component depreciation face several common obstacles. The initial componentization exercise requires significant time investment, specialized expertise, and cross-functional collaboration.

Primary implementation challenges include:

- Determining appropriate component classifications for diverse asset types

- Allocating historical asset costs when original component details are unavailable

- Establishing reliable useful life estimates without extensive operational data

- Training accounting staff on new systems and methodologies

- Integrating component tracking with existing ERP and asset management systems

Successful implementations typically involve phased approaches, starting with new asset acquisitions before retroactively componentizing existing assets. Detailed guidance on the component depreciation method provides practical frameworks for addressing these challenges systematically.

Technology Solutions for Component Management

Modern enterprise resource planning systems increasingly support component depreciation natively, but many organizations still rely on spreadsheets or manual processes. Technology investment in this area delivers substantial returns through reduced errors, improved compliance, and enhanced analytical capabilities.

Comprehensive fixed asset management systems offer component-level tracking, automated depreciation calculations across multiple methods, and integration with general ledger systems. These platforms support complex scenarios including partial component disposals, separate component revaluations, and component transfer between assets.

Automation and Process Optimization

Organizations implementing automation in accounts payable and asset management can extend these efficiencies to component depreciation tracking. Automated workflows ensure consistent component identification, standardized cost allocation methodologies, and error-free depreciation calculations.

Technology-enabled capabilities include:

- Automated component classification using machine learning algorithms

- Integration with procurement systems for automatic componentization at acquisition

- Predictive analytics for component replacement timing based on depreciation patterns

- Mobile applications for field technicians to report component condition data

- Dashboard visualization of component depreciation trends and replacement forecasts

When evaluating technology solutions, organizations should prioritize platforms offering flexible configuration to accommodate industry-specific componentization requirements and scalable architecture to support growth in asset portfolios.

Practical Guidance for Different Industries

Component depreciation application varies significantly across industries based on asset characteristics, regulatory requirements, and operational priorities. Understanding industry-specific best practices enhances implementation effectiveness.

Manufacturing organizations typically componentize production equipment based on mechanical, electrical, and control system elements. Healthcare facilities focus on medical equipment components with distinct technology refresh cycles. Real estate companies emphasize building system components with varying maintenance requirements.

Healthcare Sector Applications

Healthcare organizations manage particularly complex asset portfolios requiring sophisticated componentization. Medical imaging equipment, surgical robots, and diagnostic systems contain expensive technology components with rapid obsolescence alongside durable mechanical structures with decades-long useful lives.

Healthcare revenue cycle optimization depends on accurate equipment cost tracking for proper charge capture and reimbursement. Component depreciation enables precise cost-per-procedure calculations, supporting pricing strategies and profitability analysis at the service line level.

Medicare cost reporting requirements add complexity, as hospitals must allocate costs appropriately across departments and service categories. Component-level depreciation provides the granularity needed for defensible cost allocation supporting reimbursement claims.

Manufacturing and Industrial Applications

Manufacturing environments benefit significantly from component depreciation given the complexity and capital intensity of production equipment. CNC machines, robotic systems, and processing lines comprise numerous components with distinct replacement cycles.

Typical manufacturing componentization patterns:

- Structural frames and housing: 20-30 year useful lives, minimal technological obsolescence

- Mechanical drive systems: 10-15 year lives, wear-based replacement needs

- Electronic controls and sensors: 5-8 year lives, technology-driven upgrades

- Software and programming: 3-5 year lives, frequent updates and enhancements

This granular tracking supports total productive maintenance programs by aligning financial depreciation schedules with preventive maintenance plans and component replacement strategies.

Integration with Broader Financial Strategy

Component depreciation functions as one element within comprehensive asset management and financial planning frameworks. Organizations maximize value by integrating componentization with capital budgeting, cash flow forecasting, and performance measurement systems.

Achieving growth and efficiency in operations requires aligning financial reporting practices with operational realities. Component depreciation provides the foundation for this alignment by ensuring accounting systems reflect actual asset consumption patterns.

Capital Planning and Budgeting

Component-level depreciation data transforms capital planning from reactive replacement of failed equipment to proactive lifecycle management. Finance teams can forecast replacement needs years in advance based on component depreciation schedules, enabling better cash flow management and funding strategy development.

Organizations should develop rolling five-year capital plans incorporating component replacement forecasts derived from depreciation tracking. This forward-looking approach prevents budgetary surprises and supports strategic decisions about repair-versus-replace trade-offs.

Capital planning integration steps:

- Extract component depreciation schedules for all major asset categories

- Analyze historical replacement patterns to validate useful life assumptions

- Develop probabilistic models for component failure before full depreciation

- Create funding strategies addressing bunched replacement requirements

- Monitor actual component performance against depreciation assumptions

The componentization framework also supports lease-versus-buy analyses by providing accurate total cost of ownership calculations incorporating realistic component replacement timing rather than simplified straight-line assumptions.

Component depreciation represents more than an accounting technicality-it's a strategic tool enabling organizations to manage assets more effectively, plan capital investments more accurately, and report financial results more transparently. By recognizing that complex assets comprise multiple components with distinct lifecycles, organizations gain visibility into true operational costs and replacement timing that drives better decision-making across finance, operations, and strategic planning functions. Nero and Associates, Inc. helps organizations implement sophisticated financial management practices, automate manual processes, and optimize operational efficiency through our performance-based consulting approach that delivers measurable results in cost savings, time efficiency, and employee wellness.