Tax planning represents one of the most powerful levers organizations can pull to improve financial performance and operational efficiency. Among the various tax strategies available to businesses, accelerated depreciation stands out as a particularly effective method for reducing taxable income while maintaining healthy cash flow. This approach allows companies to recognize larger depreciation deductions in the early years of an asset's useful life, creating immediate tax savings that can be reinvested into growth initiatives, technology upgrades, or employee development programs. For organizations focused on operational excellence and bottom-line improvement, understanding and implementing accelerated depreciation strategies can yield significant financial benefits.

Understanding the Fundamentals of Accelerated Depreciation

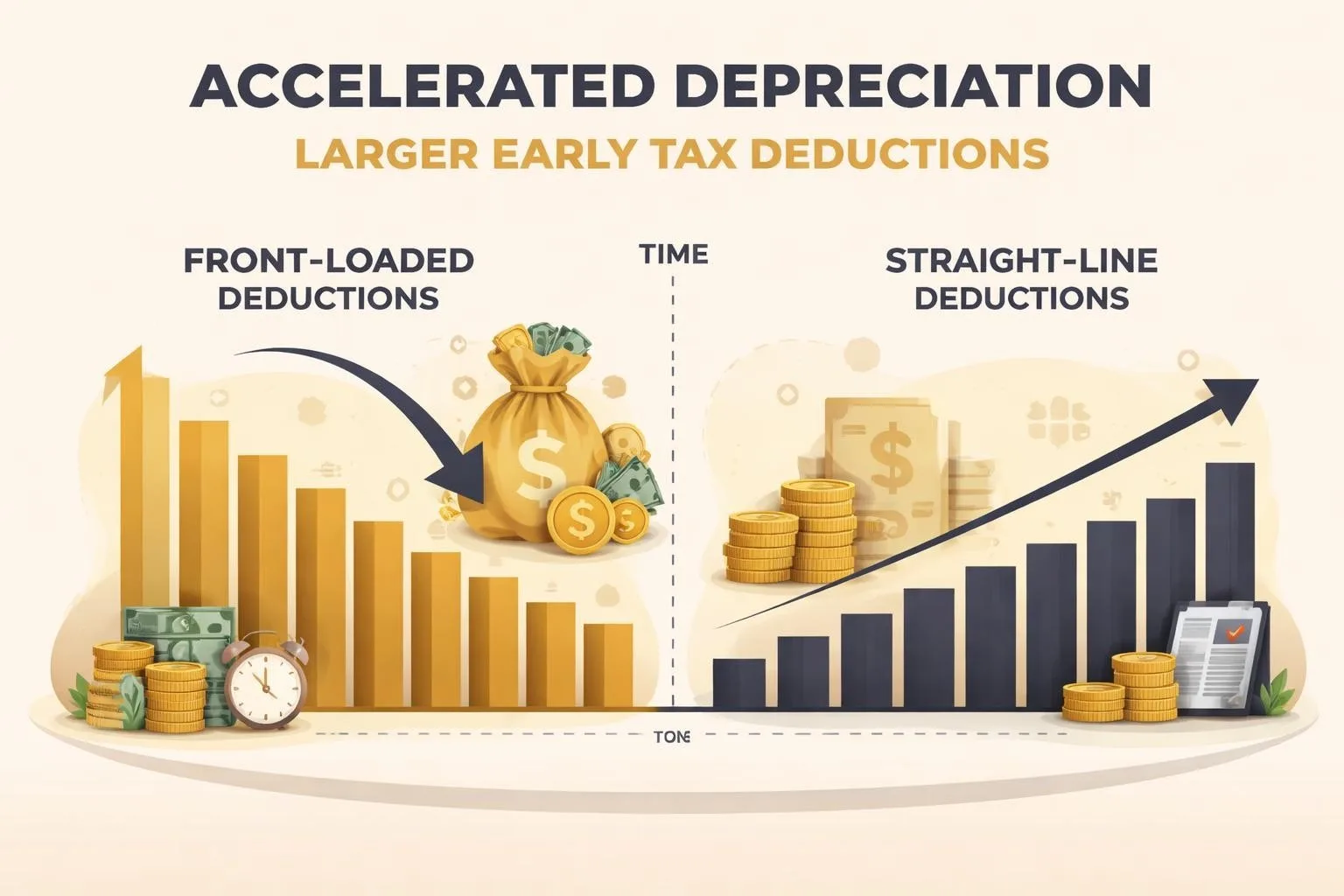

Accelerated depreciation is a tax accounting method that enables businesses to deduct a larger portion of an asset's cost during the initial years following its acquisition. Unlike straight-line depreciation, which spreads the deduction evenly over an asset's useful life, this approach front-loads the tax benefit.

The primary advantage centers on the time value of money. A dollar saved in taxes today holds more value than the same dollar saved five years from now. By claiming larger deductions earlier, businesses reduce their current tax liability and free up capital for immediate operational needs.

The Modified Accelerated Cost Recovery System (MACRS)

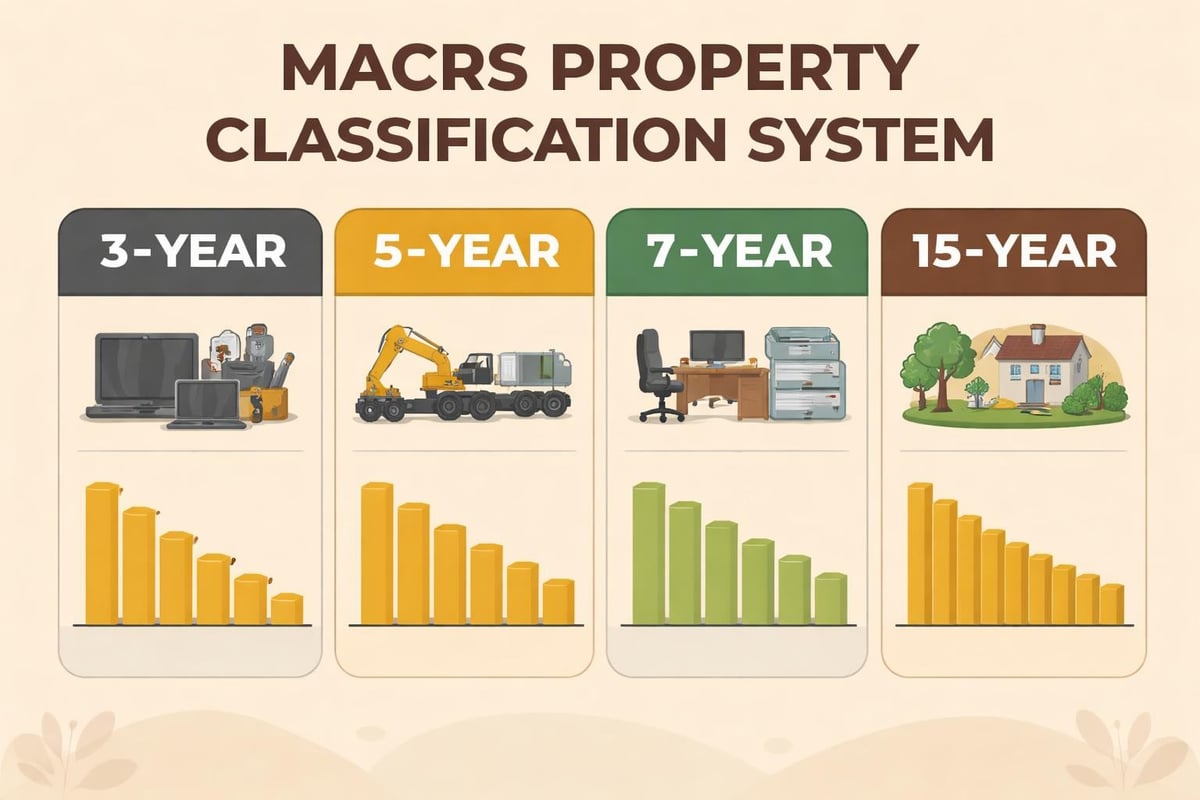

The Modified Accelerated Cost Recovery System serves as the foundation for most depreciation calculations in the United States. Implemented through tax code revisions, MACRS establishes specific recovery periods and depreciation methods for different asset categories.

MACRS categorizes assets into property classes:

- 3-year property (special tools, tractors)

- 5-year property (computers, office equipment, automobiles)

- 7-year property (office furniture, fixtures)

- 15-year property (land improvements, infrastructure)

- 27.5-year property (residential rental property)

- 39-year property (commercial real estate)

Each category follows predetermined depreciation schedules that dictate the percentage of cost recoverable each year. For most tangible personal property, the 200% declining balance method applies, which doubles the straight-line depreciation rate.

Depreciation Methods Under Accelerated Systems

Organizations implementing accelerated depreciation strategies typically choose between several calculation methods, each offering distinct advantages depending on asset type and business objectives.

Double Declining Balance Method

The double declining balance method represents the most aggressive approach to accelerated depreciation. This calculation multiplies the straight-line depreciation rate by two, then applies that percentage to the asset's remaining book value each year.

Calculation example for a $100,000 asset with a 5-year recovery period:

| Year | Beginning Value | Depreciation Rate | Annual Deduction | Ending Value |

|---|---|---|---|---|

| 1 | $100,000 | 40% | $40,000 | $60,000 |

| 2 | $60,000 | 40% | $24,000 | $36,000 |

| 3 | $36,000 | 40% | $14,400 | $21,600 |

| 4 | $21,600 | 40% | $8,640 | $12,960 |

| 5 | $12,960 | Switch to straight-line | $12,960 | $0 |

The declining balance method automatically switches to straight-line depreciation when that method provides a larger deduction, maximizing tax benefits throughout the asset's life.

150% Declining Balance Method

For certain property types, IRS Publication 946 permits the use of a 150% declining balance rate rather than 200%. This method applies primarily to 15-year and 20-year property, offering a moderate acceleration compared to the double declining balance approach.

This calculation multiplies the straight-line rate by 1.5, creating a depreciation schedule that falls between the aggressive double declining balance method and traditional straight-line depreciation.

Bonus Depreciation and Section 179 Deductions

Beyond standard MACRS calculations, businesses can leverage additional first-year deduction opportunities that dramatically accelerate cost recovery.

Bonus Depreciation Provisions

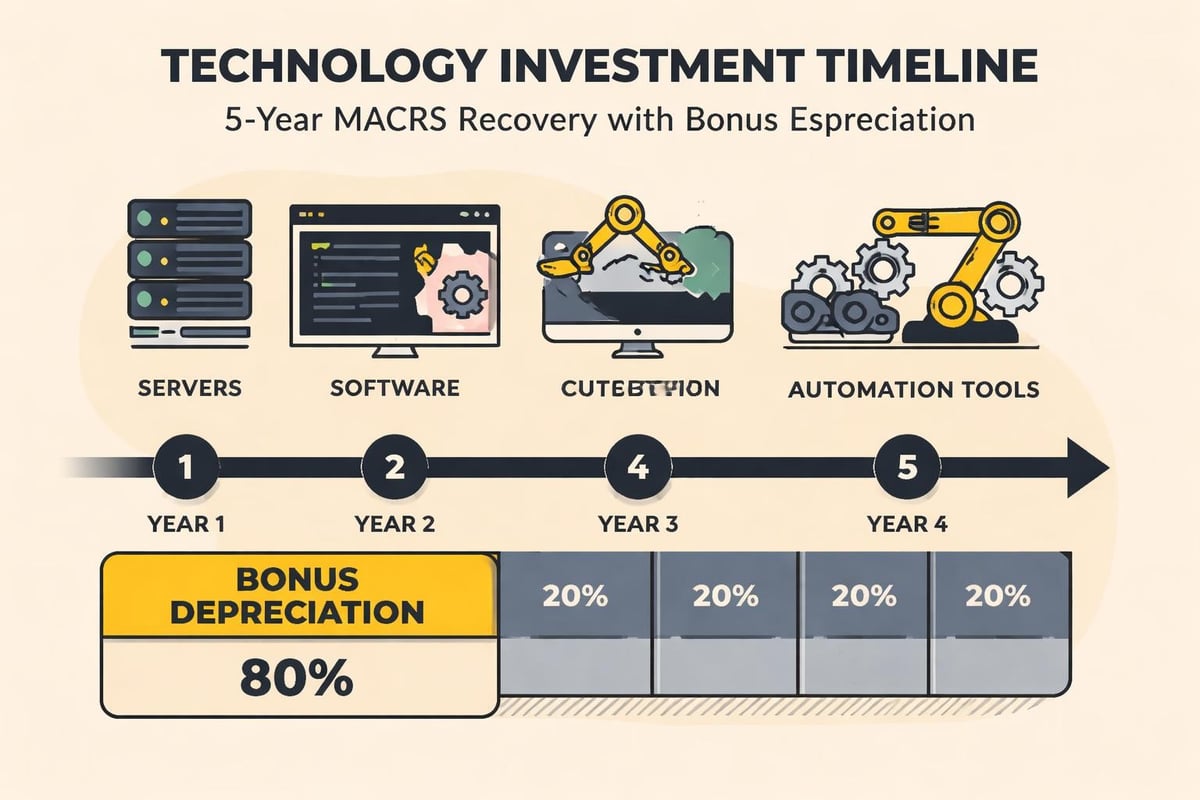

Bonus depreciation allows businesses to immediately deduct a significant percentage of qualifying property costs in the year of acquisition. As of 2026, the bonus depreciation percentage phases down from previous levels, but still provides substantial benefits.

Qualifying property requirements:

- Original use must begin with the taxpayer

- Property must have a recovery period of 20 years or less

- Acquisition must meet specific timing requirements

- Property cannot be listed property used 50% or less for business

For organizations investing heavily in automation technology, AI systems, or integration platforms, bonus depreciation creates immediate tax savings that can offset implementation costs. This proves particularly valuable for consultancies focused on operational efficiency that regularly upgrade technological infrastructure.

Section 179 Expensing Limitations

Section 179 permits businesses to immediately expense qualifying equipment purchases up to annual limits. For 2026, these limits continue to adjust for inflation, providing substantial first-year deductions.

Unlike bonus depreciation, Section 179 includes phase-out thresholds that reduce available deductions once total equipment purchases exceed specified amounts. This makes the provision most beneficial for small to mid-sized businesses making moderate equipment investments.

| Feature | Section 179 | Bonus Depreciation |

|---|---|---|

| Maximum deduction | Subject to annual limits | Percentage of cost |

| Phase-out threshold | Yes | No |

| Used property | Eligible (with conditions) | Limited eligibility |

| Income limitation | Cannot create loss | Can create loss |

Strategic Applications for Service Organizations

Professional services firms face unique depreciation planning opportunities, particularly when investing in technology infrastructure that enhances service delivery and operational efficiency.

Technology Infrastructure Investments

Companies implementing AI automation and integration solutions frequently purchase substantial computer equipment, software, and supporting infrastructure. These assets typically qualify as 5-year property under MACRS, making them ideal candidates for accelerated depreciation strategies.

Computer servers, workstations, networking equipment, and enterprise software installations all benefit from front-loaded deductions. For organizations expanding their technological capabilities, the combination of MACRS acceleration, bonus depreciation, and Section 179 can create significant first-year tax savings.

Office and Operational Asset Planning

Beyond technology, service organizations invest in furniture, fixtures, leasehold improvements, and specialized equipment. Each category follows specific recovery periods that affect depreciation strategy.

Office furniture and fixtures typically fall into the 7-year property class, while qualified leasehold improvements may qualify for shorter recovery periods. Strategic timing of these purchases can maximize tax benefits, particularly when combined with bonus depreciation provisions.

Impact on Cash Flow and Financial Planning

The relationship between accelerated depreciation and cash flow management deserves careful consideration, as tax savings directly translate into available operating capital.

Cash Flow Enhancement Through Tax Savings

Every dollar of accelerated depreciation reduces taxable income, creating immediate cash savings equal to the deduction multiplied by the marginal tax rate. For a business in the 21% federal corporate tax bracket, a $100,000 first-year depreciation deduction generates $21,000 in tax savings.

These savings remain with the business rather than flowing to tax authorities, providing capital for:

- Hiring and training initiatives that improve employee capabilities

- Additional technology investments that enhance operational efficiency

- Working capital reserves that support business expansion

- Healthcare and wellness programs that benefit workforce health

Organizations focused on optimizing operational costs recognize that accelerated depreciation represents one component of comprehensive financial management strategies.

Book-Tax Differences and Financial Reporting

Businesses must navigate the distinction between tax depreciation and financial statement depreciation. While accelerated methods maximize tax benefits, financial reporting often employs straight-line depreciation to present consistent earnings.

Key considerations for managing book-tax differences:

- Deferred tax liabilities arise from temporary timing differences

- Financial statements require disclosure of depreciation methods

- Cash flow statements reflect actual tax savings regardless of book method

- Long-term planning must account for depreciation reversals in later years

Economic Research and Policy Considerations

Academic research has explored how depreciation policies influence business investment decisions and broader economic activity. Studies examining macroeconomic effects suggest that accelerated depreciation can stimulate capital investment during economic expansion periods.

Policy makers periodically adjust depreciation provisions to encourage specific types of investment or stimulate economic growth. Businesses benefit from monitoring legislative changes that could affect available deductions or modify existing recovery periods.

Planning for Depreciation Phase-Outs

Certain accelerated depreciation provisions include scheduled phase-downs or sunset dates. The bonus depreciation percentage, for instance, follows a predetermined reduction schedule unless extended by legislation.

Organizations developing multi-year capital investment plans should consider these phase-downs when timing major acquisitions. Accelerating purchases before provision reductions can maximize available tax benefits.

Integration with Broader Business Strategies

Accelerated depreciation achieves maximum impact when integrated with comprehensive operational and financial planning frameworks.

Coordinating Depreciation with Revenue Optimization

For organizations managing healthcare revenue cycles, depreciation planning intersects with equipment investment decisions that directly affect revenue generation capabilities. Medical equipment, billing systems, and patient management technology all generate depreciation deductions while simultaneously supporting revenue operations.

The strategic timing of such investments considers not only tax benefits but also operational readiness, training requirements, and implementation timelines that affect revenue realization.

Aligning Depreciation with Growth Initiatives

Businesses experiencing rapid growth face unique depreciation planning opportunities. As SMBs scale operations, equipment needs expand proportionally, creating larger depreciation pools that generate substantial tax savings.

Growth-focused organizations benefit from developing capital investment calendars that optimize depreciation benefits while meeting operational requirements. This approach ensures that tax considerations complement rather than drive business decisions.

Asset Disposition and Recapture Considerations

Understanding what happens when disposing of depreciated assets completes the accelerated depreciation planning picture. Tax law requires recapture of excess depreciation when assets sell for amounts exceeding their depreciated basis.

Depreciation Recapture Mechanics

If a business sells an asset for more than its tax basis (original cost minus accumulated depreciation), the gain receives special treatment. The portion representing depreciation deductions becomes ordinary income subject to recapture rules.

Example recapture calculation:

- Original equipment cost: $50,000

- Accumulated depreciation: $40,000

- Current tax basis: $10,000

- Sale price: $25,000

- Total gain: $15,000 (with depreciation recapture rules applying)

This recapture requirement doesn't eliminate the benefit of accelerated depreciation but rather defers a portion of the tax benefit until asset disposition. The time value of money typically makes early deductions worthwhile despite eventual recapture.

Like-Kind Exchange Considerations

Certain asset exchanges allow businesses to defer depreciation recapture through like-kind exchange provisions. These transactions require careful structuring and apply to limited property types under current tax law.

For service organizations regularly upgrading equipment, understanding like-kind exchange rules helps minimize immediate tax consequences while maintaining the benefits of accelerated depreciation on replacement property.

Implementation Best Practices

Successfully leveraging accelerated depreciation requires systematic approaches to asset tracking, tax compliance, and strategic planning.

Establishing Asset Management Systems

Effective depreciation management begins with robust asset tracking that captures acquisition dates, costs, classifications, and recovery periods. Modern accounting systems automate these calculations, but businesses must ensure accurate initial data entry.

Essential asset management components:

- Detailed purchase documentation with acquisition dates

- Proper asset classification according to IRS guidelines

- Tracking of bonus depreciation and Section 179 elections

- Coordination between financial and tax reporting systems

- Regular reconciliation of asset registers with tax returns

Organizations implementing automation and integration solutions can leverage technology to streamline asset management processes, reducing manual effort while improving accuracy.

Coordinating with Tax Professionals

While general depreciation concepts remain consistent, specific applications vary based on industry, asset type, and business circumstances. Engaging qualified tax advisors ensures compliance while maximizing available benefits.

Tax professionals help businesses navigate complex scenarios involving mixed-use property, bonus depreciation elections, and coordination of federal and state depreciation rules. Their expertise proves particularly valuable when evaluating major capital investments or business acquisitions.

Accelerated depreciation represents a powerful tool for businesses seeking to optimize tax outcomes while maintaining strong cash flow positions. By understanding MACRS methodologies, bonus depreciation provisions, and strategic timing considerations, organizations can significantly reduce current tax burdens and reinvest savings into operational improvements. Nero and Associates, Inc. helps organizations implement comprehensive financial strategies that integrate tax planning with operational excellence, automation initiatives, and employee wellness programs. Our performance-based approach ensures that depreciation strategies align with broader business objectives while delivering measurable bottom-line improvements.