Imagine being admitted to the hospital unexpectedly. Are you confident your health insurance alone will protect you from all the costs that follow?

This 2026 Hospital Indemnity Guide is here to clarify what hospital indemnity really offers, how it works, and why it can be a financial lifesaver for individuals and families.

You will learn what hospital indemnity insurance is, the benefits it provides, who should consider it, and how to choose the right plan for your needs.

Prepare to understand the true risks of hospital costs, discover how this coverage brings peace of mind, and get practical steps to make informed decisions about your financial health.

Understanding Hospital Indemnity Insurance

Navigating hospital bills can be overwhelming. To make informed decisions, it is crucial to understand what hospital indemnity insurance is, how it operates, and how it fits with other coverage.

What Is Hospital Indemnity Insurance?

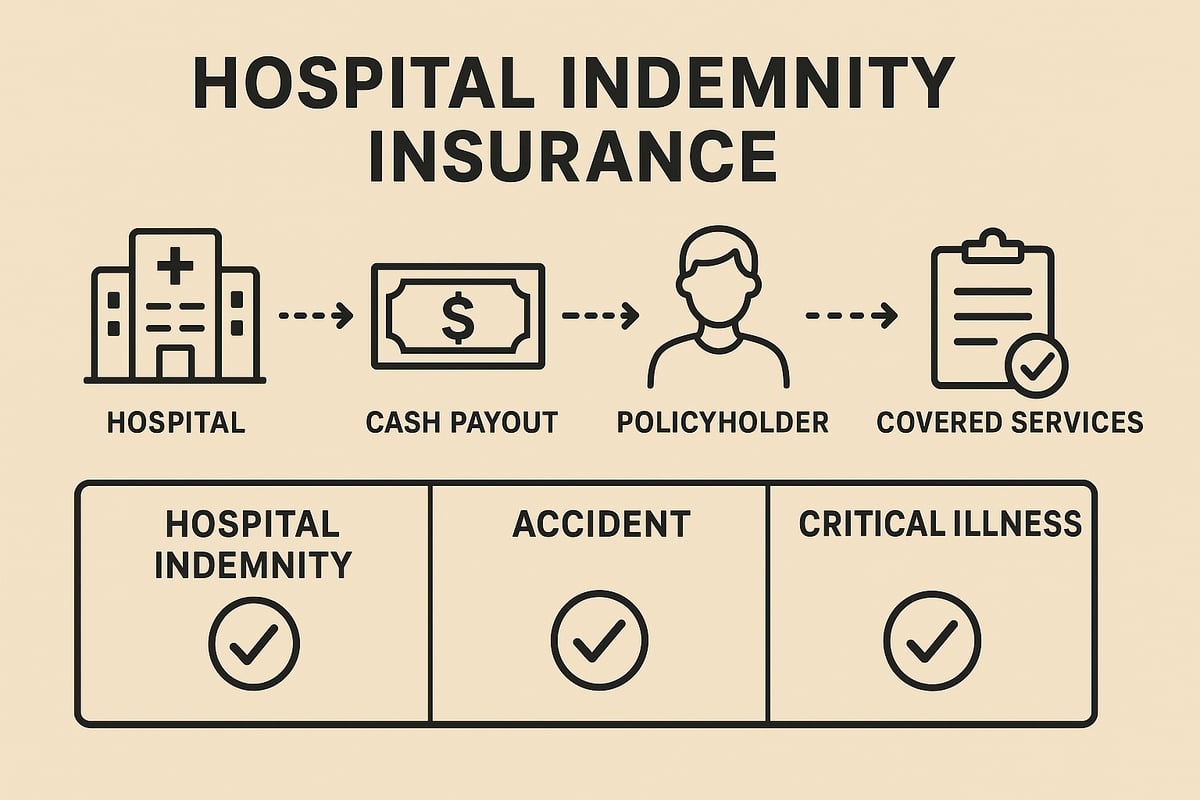

Hospital indemnity insurance is a supplemental policy that pays you cash benefits if you are admitted to the hospital. Unlike traditional health insurance, which pays providers directly, hospital indemnity pays the policyholder, regardless of the actual medical costs.

The main goal is to help cover out-of-pocket expenses, such as deductibles, coinsurance, or even everyday bills. For example, if you are hospitalized, you may receive a set cash amount for each day you stay.

According to major insurers, this cash is flexible and can be used for any need. For a deeper look, see What is a health indemnity plan.

This flexibility provides peace of mind during medical emergencies.

How Does Hospital Indemnity Insurance Work?

Hospital indemnity coverage is based on a monthly premium. You pay a set amount, and in return, you are eligible to receive a cash payout if hospitalized.

Most plans pay either a lump sum or a daily benefit, regardless of your actual hospital bills. There are typically no provider network restrictions, so you can use any hospital.

Unlike many health plans, there are usually no deductibles to meet before benefits start. For example, if you are admitted for three days, you receive payment for each day, often within days of submitting a claim.

Most policies pay based on the number of days you are hospitalized.

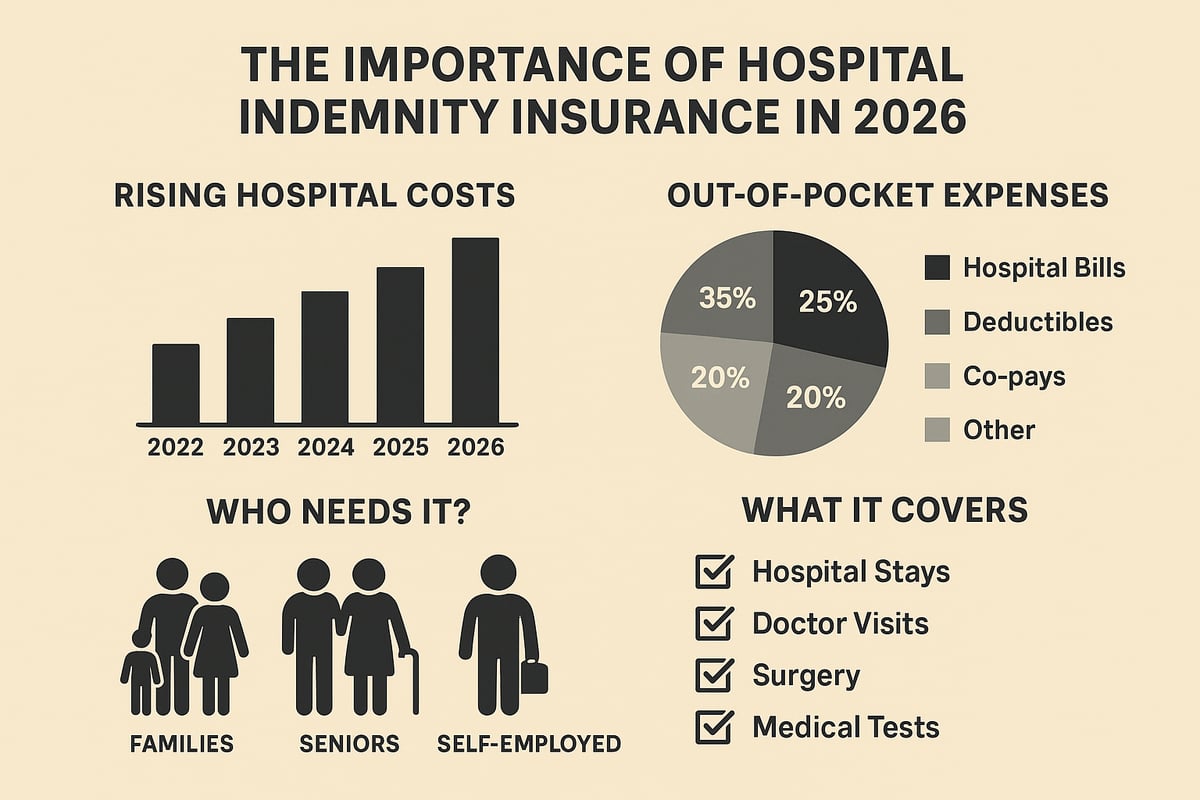

What Does Hospital Indemnity Insurance Cover?

Hospital indemnity policies generally cover a range of hospital-related scenarios. Common covered events include:

- Hospital admissions (with or without surgery)

- Intensive care or critical care unit stays

- Outpatient surgery (with some higher-tier plans)

- Emergency room and ambulance services (varies by plan)

- Childbirth and postnatal hospital stays

For example, some plans offer broader coverage if you pay a higher premium. This might include outpatient surgeries or additional services. Always check your policy details for specific covered events.

Coverage is designed to help ease the financial burden during recovery.

Key Differences Compared to Other Supplemental Plans

Hospital indemnity insurance stands apart from accident or critical illness policies. The main distinction is in what triggers the benefit and how payments are made.

| Feature | Hospital Indemnity | Accident Insurance | Critical Illness Insurance |

|---|---|---|---|

| Trigger Event | Hospitalization | Injury from accident | Diagnosis of covered illness |

| Payment Structure | Per day/lump sum | Lump sum | Lump sum |

| Usage Flexibility | Any purpose | Any purpose | Any purpose |

For example, accident insurance helps with injuries, while hospital indemnity pays for any hospital stay, regardless of cause. This makes hospital indemnity a valuable complement to other supplemental coverage, not a replacement.

Common Misconceptions and FAQs

A common misconception is that health insurance covers all hospital expenses. In reality, out-of-pocket costs, deductibles, and living expenses can add up quickly.

Frequently asked questions include:

- Do plans pay a lump sum or daily benefit?

- Is family coverage available?

- Are there age or health restrictions?

For instance, many plans let you add family members, but eligibility varies. Hospital stays can result in thousands in out-of-pocket costs, even for those with good insurance.

Understanding these facts can help you make informed choices about hospital indemnity coverage.

Why Hospital Indemnity Insurance Matters in 2026

Unexpected hospital bills can disrupt any household budget, regardless of how prepared you think you are. While health insurance is essential, gaps in coverage often leave individuals and families exposed to significant expenses. Understanding why hospital indemnity insurance stands out in 2026 can help you make smarter choices for your financial well-being.

Rising Healthcare Costs and Coverage Gaps

Healthcare expenses in the United States continue to rise, outpacing wage growth and household savings. The average out-of-pocket cost for a hospital stay now exceeds $1,200, even for those with solid health insurance. Deductibles and coinsurance have steadily increased, making it harder for people to predict their actual financial responsibility after a hospital admission.

According to the Milliman Hospital Indemnity Survey 2025, demand for hospital indemnity insurance is growing as more people recognize these coverage gaps. Even with strong primary insurance, a single hospital visit can lead to unplanned bills. Hospital indemnity provides an extra layer of protection, ensuring you are not caught off guard by escalating costs.

Who Should Consider Hospital Indemnity Insurance?

Hospital indemnity is not just for those with chronic conditions or frequent hospitalizations. It is a valuable tool for families planning for childbirth, older adults facing increased health risks, and individuals with high-deductible health plans. Self-employed professionals and gig workers, who may lack comprehensive employer benefits, also find hospital indemnity especially useful.

For example, growing families can use hospital indemnity to offset the costs of maternity stays, while seniors benefit from additional financial security during unexpected illnesses. Reviewing your current health status, lifestyle, and risk factors can help determine if hospital indemnity fits your needs.

Financial Protection and Peace of Mind

One of the greatest strengths of hospital indemnity is its ability to reduce financial stress during recovery. Instead of worrying about how to pay for deductibles, rent, or groceries, policyholders receive direct cash benefits. This flexibility allows you to focus on healing and supporting your loved ones, rather than managing mounting bills.

MetLife and other major insurers highlight that hospital indemnity cash can be used for any purpose, from childcare to transportation. This freedom empowers individuals and families to make the best decisions for their unique situations, providing peace of mind that goes beyond numbers on a bill.

Real-Life Scenarios and Case Studies

Consider a family with a high-deductible plan who faces a $3,000 bill after childbirth. Their hospital indemnity policy covers a significant portion, easing the burden. In another scenario, a senior hospitalized for pneumonia uses the cash benefit to pay for rent and prescription medications during recovery.

Thousands of hospital indemnity policyholders have avoided debt by leveraging these supplemental benefits. The real-world impact is clear: hospital indemnity can be the difference between financial stability and hardship after a health crisis.

Limitations and Exclusions to Consider

While hospital indemnity offers broad protection, it is important to understand its limits. Most plans have pre-existing condition waiting periods, coverage caps per hospital stay or per year, and specific exclusions. Common exclusions include cosmetic surgery and certain outpatient procedures.

Carefully review policy details before enrolling. For example, some plans limit the number of payable days per hospital admission, which could affect your benefit if you experience a prolonged stay. Knowing these details ensures you maximize your hospital indemnity coverage and avoid surprises.

Key Features and Benefits of Hospital Indemnity Insurance

Hospital indemnity insurance stands out for its unique set of features that provide both financial security and peace of mind. Understanding these benefits can help you make an informed decision about how hospital indemnity fits into your overall health and financial planning.

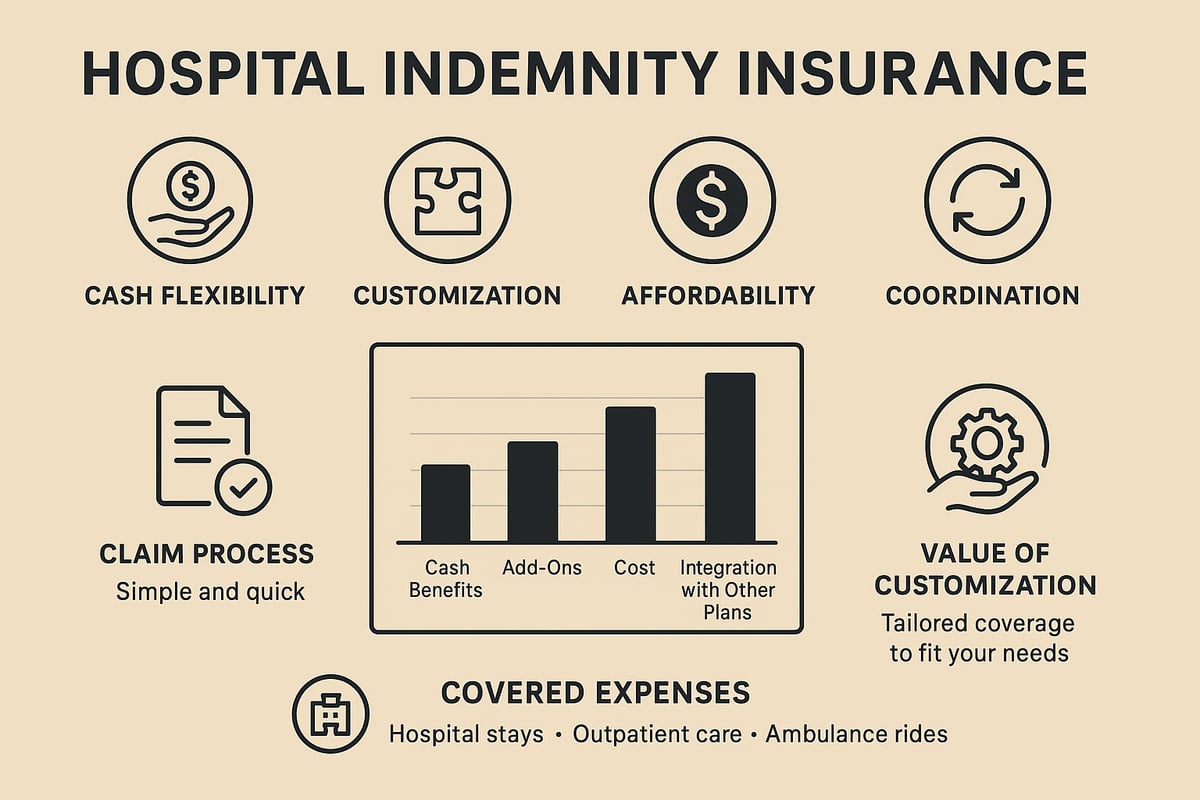

Flexibility and Use of Cash Benefits

One of the standout features of hospital indemnity is its remarkable flexibility. When you receive a benefit from your hospital indemnity policy, the cash goes directly to you, not to a hospital or provider. This means you decide how to use the money.

Policyholders often use these funds to cover household bills, mortgage payments, or transportation costs during recovery. There are no restrictions on how you spend your hospital indemnity payout. For example, if you are out of work after a hospital stay, the benefit can bridge income gaps or help pay for childcare. This flexibility empowers you to manage both medical and non-medical expenses during a challenging time.

Coverage Customization and Add-Ons

Hospital indemnity plans are highly customizable, allowing you to tailor coverage to your unique needs. Many providers offer options to add family members or select riders for intensive care, surgical procedures, or additional services.

You can choose from varying benefit levels based on your budget and risk profile. For instance, higher premium plans might include outpatient surgery or emergency room visits. Industry leaders are continually enhancing their offerings. For example, Guardian’s Enhanced Hospital Indemnity Benefits reflect a growing trend toward more innovative and comprehensive customization. This adaptability ensures your hospital indemnity coverage stays relevant as your life changes.

Affordability and Value

Affordability is a key reason many people consider hospital indemnity as part of their financial safety net. Monthly premiums are usually lower than those for other supplemental insurance types, making this coverage accessible for a wide range of budgets.

The value becomes clear when you compare a modest monthly premium to the potential out-of-pocket expenses from a hospital stay. For families and individuals with high-deductible health plans, hospital indemnity can offer significant savings. Most people find that the cost-benefit ratio is favorable, especially if they are at higher risk for hospitalization or have dependents who may need coverage.

Coordination with Other Insurance Plans

Hospital indemnity is designed to work seamlessly alongside your primary health insurance. It does not interfere with your existing health plan benefits or claims. Instead, it supplements your coverage, providing an extra layer of financial protection.

Many policyholders use hospital indemnity benefits to cover deductibles, coinsurance, or expenses that health savings accounts do not fully address. This strategic coordination maximizes your total healthcare coverage without overlap. As a result, you gain more comprehensive protection and can focus on recovery rather than worrying about unexpected costs.

How to Choose the Right Hospital Indemnity Plan in 2026

Choosing the right hospital indemnity plan can feel overwhelming, but a clear, step-by-step approach helps ensure your decision aligns with your unique needs. In 2026, understanding your options and requirements is more important than ever. Let’s break down the process into manageable steps so you can feel confident in your hospital indemnity selection.

Assessing Your Needs and Risk Factors

Begin by taking stock of your personal and family health profile. Consider your age, medical history, and the likelihood of facing a hospital stay in the near future. Are you planning for childbirth, managing a chronic condition, or approaching retirement? Each scenario influences what you’ll need from a hospital indemnity plan.

Evaluate your financial situation as well. If a sudden hospital bill would strain your budget, hospital indemnity coverage can be a critical safety net. Think about dependents, income stability, and any existing health insurance gaps. Tailoring your choice to your risk factors ensures you get the right level of protection.

Comparing Plan Features and Costs

Hospital indemnity offerings vary widely. Carefully compare benefit amounts, monthly premiums, and the specific services covered by each plan. Some plans may cover only inpatient stays, while others include outpatient procedures or emergency care for higher premiums.

Use a table to organize your findings:

| Feature | Plan A | Plan B |

|---|---|---|

| Monthly Premium | $20 | $35 |

| Daily Hospital Benefit | $200 | $300 |

| Outpatient Surgery Cover | No | Yes |

| Family Coverage | Optional | Included |

Look for a hospital indemnity plan that balances affordability with the coverage you need. Reading the fine print on exclusions and waiting periods will help you avoid surprises later.

Questions to Ask Before Enrolling

Before committing to any hospital indemnity plan, prepare a list of essential questions:

- How soon are benefits paid after hospital admission?

- What is the maximum number of covered days per admission?

- Are dependents covered, and what is the additional cost?

- Are there age or health restrictions?

- Does the plan offer a lump sum or daily benefit payment?

Asking these questions ensures you fully understand your policy’s terms. Confirm how claims are filed and if there are any pre-existing condition limitations. This proactive approach helps you avoid unexpected gaps in your hospital indemnity coverage.

Understanding Enrollment and Eligibility

Enrollment options for hospital indemnity plans can differ. Some are available only during open enrollment periods, while others can be purchased year-round. Employer-sponsored plans may have different rules than individual policies.

Many hospital indemnity plans do not require a medical exam, and most adults, along with their dependents, are eligible. If you’re considering workplace benefits, you may find additional insights on employee benefit plan design to help you evaluate your options. Always review eligibility and underwriting requirements before applying.

Steps to Enroll in a Hospital Indemnity Plan

Enrolling in a hospital indemnity plan is straightforward if you follow these steps:

- Research and compare available plans.

- Assess your personal and family needs.

- Request quotes and review policy documents carefully.

- Complete the application online, through your employer, or with an agent.

- Confirm your coverage start date and set up payment details.

Be sure to keep all documentation and confirmation emails for your records. This organized approach streamlines the process and minimizes delays in your hospital indemnity coverage.

Maximizing Benefits and Avoiding Common Pitfalls

To get the most from your hospital indemnity plan, keep your policy documents accessible and notify your insurer promptly after a hospital stay. Understand the claim filing process and meet all deadlines for submitting paperwork.

Regularly review your coverage as your life circumstances change. Many policyholders miss out on benefits simply because they’re unaware of claim procedures or coverage updates. Staying informed ensures you maximize your hospital indemnity plan’s value and avoid costly mistakes.

Hospital Indemnity Insurance and Your Overall Financial Wellness

Hospital indemnity plays a pivotal role in your financial wellness strategy. As healthcare costs climb, having a supplemental plan can help you manage unexpected expenses and protect your long-term financial goals. Understanding how hospital indemnity interacts with other insurance, reduces out-of-pocket costs, and supports your total well-being is essential for making informed decisions.

Integrating Hospital Indemnity with Other Supplemental Coverage

A comprehensive financial safety net often includes more than one type of insurance. Hospital indemnity complements accident and critical illness plans by filling gaps that primary health insurance leaves uncovered. For example, while accident insurance covers specific injuries, hospital indemnity provides cash benefits for any hospital admission, regardless of cause.

This strategic layering allows you to address a range of risks. You can combine hospital indemnity with other supplemental plans for broader protection. The flexibility of hospital indemnity means you receive payments directly, which can be used alongside other benefits.

Here’s a quick comparison:

| Insurance Type | Focus | Payment Use |

|---|---|---|

| Hospital Indemnity | Hospital stays | Any expense |

| Accident Insurance | Injuries | Medical/non-medical |

| Critical Illness | Specific illnesses | Medical/non-medical |

For more on building a holistic approach to healthcare finances, see Healthcare financial and operational excellence.

Impact on Out-of-Pocket Healthcare Costs

Hospital indemnity is designed to help offset the growing burden of out-of-pocket healthcare expenses. With deductibles and coinsurance on the rise, even a short hospital stay can drain savings. Hospital indemnity pays you directly, which can be applied to bills, copays, or even daily living costs.

Consider this: out-of-pocket maximums for individuals can reach $9,100 in 2026. Without extra coverage, many families are forced to dip into emergency funds or take on debt. Hospital indemnity mitigates these risks by providing timely cash payments when you need them most.

By reducing reliance on savings for medical bills, hospital indemnity helps you stay on track with your overall financial goals.

Supporting Mental and Physical Recovery

Financial stress after a hospital stay can slow recovery and impact mental health. Hospital indemnity alleviates this burden by giving you the freedom to focus on healing, not bills. The cash benefits can be used for anything, from home care and medication to childcare or groceries.

Families with hospital indemnity report feeling more secure during recovery periods. This peace of mind translates to better outcomes, as stress is a known factor in delayed healing. Hospital indemnity empowers you to prioritize your health and well-being, knowing you have a financial cushion in place.

Planning for the Unexpected

Hospitalization can disrupt your budget at any stage of life. Planning ahead with hospital indemnity ensures you are prepared for sudden expenses that health insurance may not fully cover. Whether it is an unexpected illness or accident, having supplemental coverage can prevent a temporary setback from becoming a long-term financial crisis.

Hospital indemnity is a smart way to safeguard your future. By integrating it into your broader financial wellness plan, you can confidently face life’s uncertainties with greater stability.

Frequently Asked Questions About Hospital Indemnity Insurance

Understanding the basics of hospital indemnity can help you make informed choices and maximize your coverage. Here, we answer the most common questions people have about these supplemental plans.

Who Qualifies for Hospital Indemnity Insurance?

Most adults are eligible for hospital indemnity, making it accessible to a wide range of individuals and families. Policies are typically available for purchase either directly from insurers or through employer benefit programs.

Eligibility criteria often include:

- Being at least 18 years old (some plans may allow dependents)

- U.S. residency or legal work status

- Meeting any plan-specific health or employment requirements

Some plans exclude those with pre-existing conditions or set age limits for new enrollees. For families, many hospital indemnity policies offer add-on coverage for spouses and children, but costs and restrictions can vary. Always review the details before enrolling to ensure your household’s needs are met.

How Are Claims Filed and Paid?

Filing a claim for hospital indemnity is designed to be straightforward and fast. After a hospital admission, you will typically need to submit a claim form along with supporting documentation, such as hospital admission and discharge papers.

The claim process generally involves:

- Notifying your insurer of the hospitalization event

- Completing and submitting the claim form

- Providing required documents (e.g., proof of admission)

- Waiting for insurer review and approval

Once approved, benefits are usually paid directly to you, not to the hospital. Many insurers process claims within a few days, so you can access your hospital indemnity cash benefit quickly and use it for any immediate expenses.

What Are Typical Exclusions and Limitations?

Hospital indemnity plans have specific exclusions and limitations you should be aware of. Common exclusions include:

- Pre-existing conditions (often subject to waiting periods)

- Elective or cosmetic surgeries

- Short hospital stays that do not meet the minimum required duration

- Non-medically necessary admissions

Coverage limits may apply to the number of days per admission or per policy year. For example, a plan might pay for up to 30 days of hospitalization annually. Always review your policy’s exclusions and benefit caps to avoid surprises when you need your hospital indemnity coverage most.

Can You Have Multiple Supplemental Plans?

Yes, you can own hospital indemnity along with other types of supplemental insurance, such as accident or critical illness plans. These policies are designed to complement each other, providing layered protection against various health-related expenses.

When you have multiple plans, you may be eligible to receive payouts from each for the same hospital event, as long as you meet the terms of each policy. This means hospital indemnity can offer valuable support alongside other benefits. For a deeper look at market growth and the evolving role of these products, see the Hospital Indemnity Insurance Market Report 2033.

Trends and Future Outlook for Hospital Indemnity Insurance

The hospital indemnity landscape is evolving rapidly in 2026. New technologies, changing regulations, and shifting consumer needs are reshaping how these supplemental plans operate and deliver value. Understanding these trends is essential for anyone considering hospital indemnity as part of their financial wellness strategy.

Evolving Coverage Options in 2026

Hospital indemnity plans now offer a broader range of features than ever before. Insurers are introducing digital claims processing, making it easier for policyholders to receive benefits quickly. Telemedicine support is becoming more common, allowing for remote consultations and faster care coordination.

Customization has also advanced, with flexible benefit structures and a wider selection of policy add-ons. According to recent market research, the number of carriers offering hospital indemnity continues to rise, reflecting strong consumer demand. For more details on this expanding market, see the U.S. Supplemental Health Market Growth report.

Regulatory and Market Changes

Regulatory updates are shaping how hospital indemnity insurance is designed and sold. In 2026, state and federal authorities are focused on increasing transparency and consumer protections. Adjustments to the Affordable Care Act and Medicaid may impact the need for supplemental coverage, especially for those with high-deductible health plans.

Insurers are adapting by revising plan disclosures and simplifying enrollment. These changes are intended to make it easier for consumers to understand their options and choose suitable coverage. As a result, hospital indemnity plans are becoming more accessible and user-friendly.

The Role of Hospital Indemnity in Employee Benefits

Employers are increasingly adding hospital indemnity to their voluntary benefits packages. This trend is especially pronounced among organizations offering high-deductible health plans, where supplemental coverage helps bridge out-of-pocket gaps.

Integration with wellness and financial health programs is also growing. Employers recognize that hospital indemnity supports both financial security and overall well-being. By providing these plans, companies help employees manage unexpected expenses and reduce financial stress during recovery.

Consumer Awareness and Education

Despite these advances, many consumers remain unaware of hospital indemnity and its benefits. Insurers and employers are investing in educational campaigns to close this gap. Clear communication about plan features, exclusions, and claims processes is essential for informed decision-making.

For readers seeking additional guidance and resources on insurance and financial wellness, visit Articles and insurance insights. Informed consumers are more likely to select plans that fit their needs and maximize their financial protection.

Predictions for the Next Five Years

Looking ahead, several trends are set to shape the future of hospital indemnity. Experts predict:

- Continued growth in enrollment as healthcare costs rise

- Increased plan customization and digital integration

- Wider adoption of AI-driven claims processing for faster payouts

- Real-time benefit tracking and mobile app management

- Hospital indemnity becoming a standard component of comprehensive financial planning

As innovations accelerate, hospital indemnity will play an even greater role in supporting both financial resilience and peace of mind.

As you’ve seen, hospital indemnity insurance can be a vital part of protecting your financial well-being and peace of mind, especially with rising healthcare costs and unexpected gaps in coverage. Whether you’re planning for your family’s future or simply want to feel more secure, having the right guidance is key. If you’d like expert advice tailored to your unique needs, I invite you to Book a Consultation. Together, we can explore options that help you safeguard your health, empower your employees, and strengthen your organization’s bottom line.