Asset management is becoming increasingly complex as we move into 2026. Organizations face rapidly shifting markets, new technologies, and evolving regulations, making asset classification more critical than ever.

Without a clear asset classification strategy, decision-making, risk management, and compliance become much more challenging. Mastering this process brings measurable benefits, from accurate reporting to optimized portfolios.

This guide explores seven essential asset classification methods. Whether you are in finance, business, or investment, you will find actionable insights to help you stay ahead in a changing landscape.

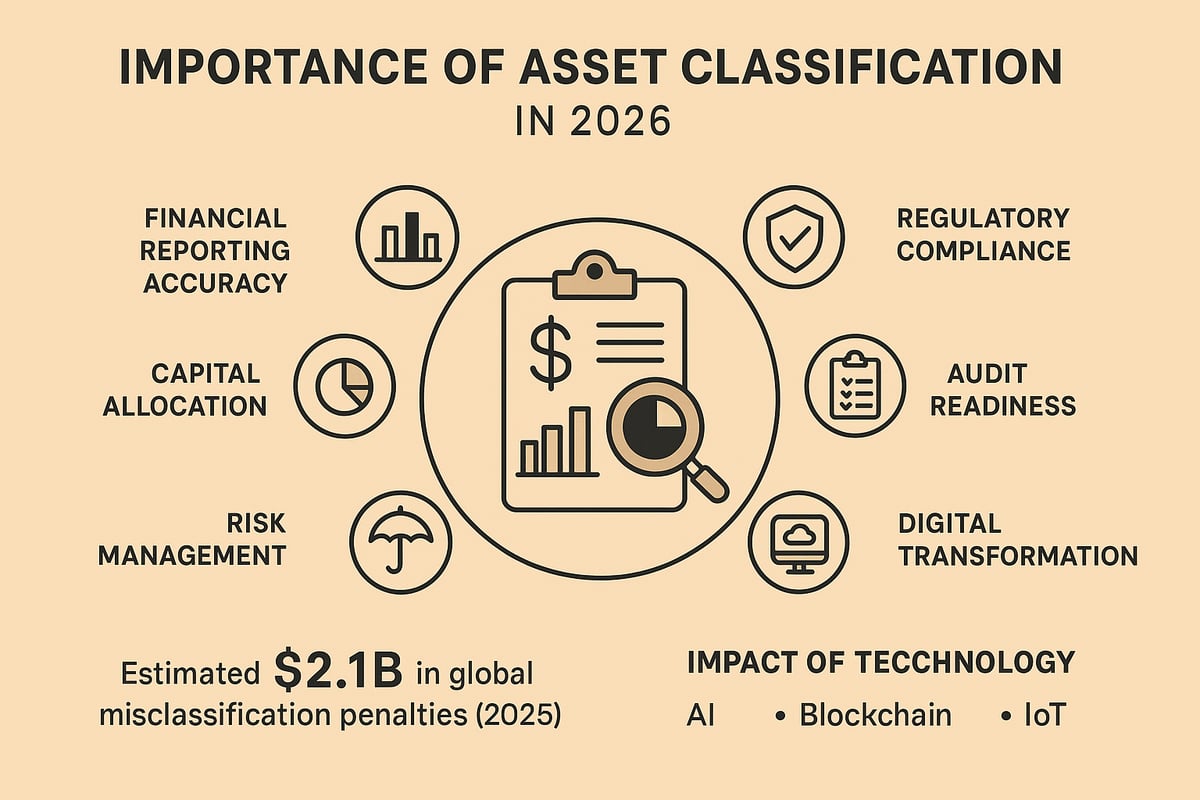

The Importance of Asset Classification in 2026

Asset classification is the backbone of modern financial and operational management. In 2026, organizations face more complex asset landscapes than ever before. With a growing range of physical and digital assets, getting asset classification right is essential to maintain transparency and control.

Effective asset classification enables accurate financial reporting, which is critical for stakeholders and regulatory bodies. It ensures that assets are correctly reflected on balance sheets, making audits more straightforward and reducing the risk of compliance issues. When assets are misclassified, organizations can face costly penalties and even legal consequences. According to recent industry reports, global companies lost an estimated $2.1 billion in 2025 due to asset misclassification and related regulatory fines.

The digital transformation sweeping across industries has brought powerful new tools for asset classification. Artificial intelligence and automation streamline the process, allowing for real-time tracking and better data accuracy. With the integration of blockchain and IoT devices, organizations can now verify asset status and location instantly. These advances help reduce manual errors and improve audit readiness.

Regulatory frameworks such as IFRS and GAAP have evolved, making asset classification more nuanced. Updates to these standards require companies to reassess how they categorize assets, especially as intangible and digital assets become more prevalent. Keeping up with regulatory changes is vital for businesses aiming to avoid compliance gaps and maintain investor trust.

Proper asset classification also supports better risk management and strategic planning. By clearly categorizing assets, companies can allocate capital more efficiently and optimize portfolio performance. For example, a multinational manufacturer improved its capital allocation by restructuring its asset categories, resulting in a 12% reduction in operational costs.

Adopting standardized asset classification practices is now a best practice across sectors. Leading organizations follow frameworks such as APPA’s asset classification standards to ensure consistency and information quality. These standards help companies benchmark their processes, enhance reporting, and support better decision-making.

As the business environment becomes increasingly dynamic, the need for agile, technology-driven asset classification systems grows. Organizations that invest in advanced classification methods and tools are better positioned to adapt to market shifts, regulatory changes, and emerging risks. In 2026, mastering asset classification is not just an administrative task—it is a strategic advantage.

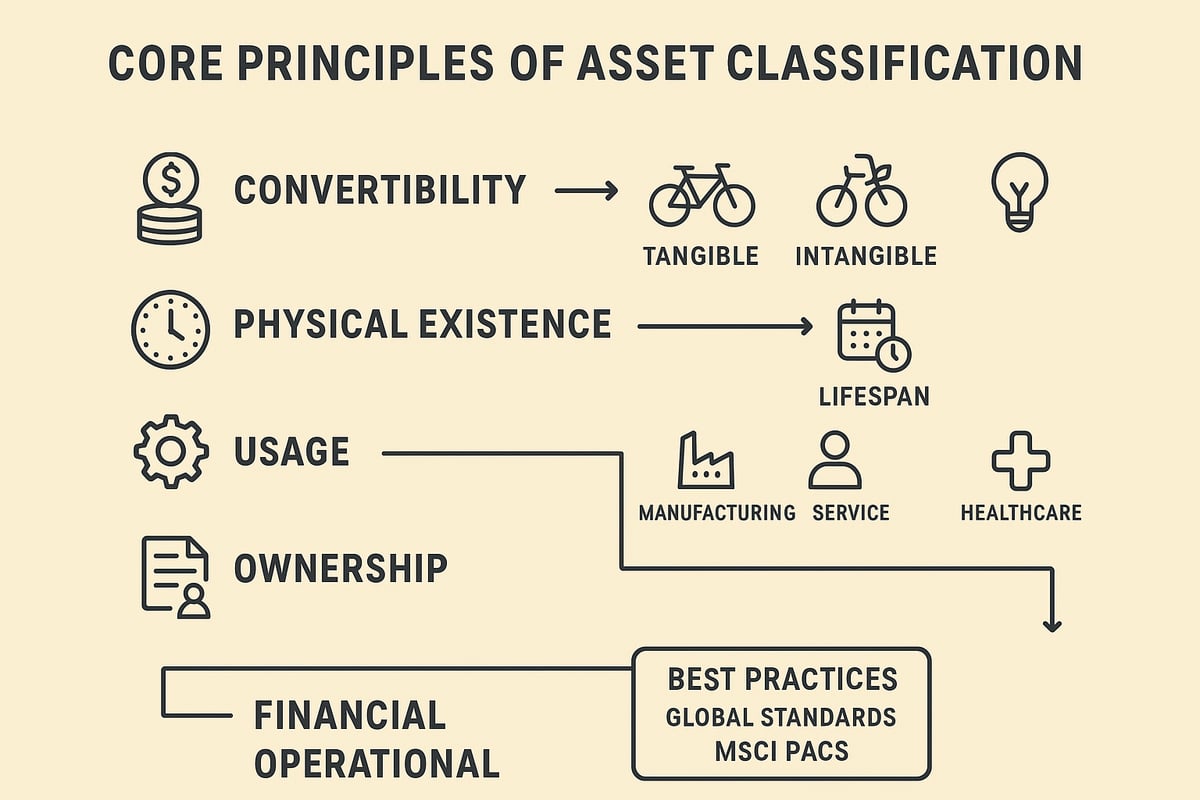

Core Principles and Criteria for Asset Classification

Asset classification is the backbone of modern financial management, providing a structured approach to organizing and evaluating assets. At its core, asset classification relies on foundational criteria such as convertibility, physical existence, usage, and ownership. Convertibility distinguishes between assets that can be quickly turned into cash and those intended for long-term use. Physical existence separates tangible items like equipment and buildings from intangible assets such as patents and software. Usage focuses on whether assets support daily operations or serve as investments, while ownership clarifies if assets are held outright or under lease agreements.

These principles are vital across different perspectives. Financial, operational, and regulatory requirements all influence how asset classification is applied within organizations. Financial reporting depends on accurate asset classification to ensure compliance with standards and support informed decision-making. Operational needs often prioritize asset liquidity and lifespan, affecting day-to-day management and investment planning. Regulatory frameworks, such as IFRS and GAAP, set strict guidelines for categorization and reporting, making it critical to align internal processes with external mandates.

Industry sector, business size, and specific asset types further shape classification strategies. For example, manufacturing firms may focus on inventory and machinery, while service-based businesses prioritize intangible assets and intellectual property. The nature of asset classification in healthcare, technology, or infrastructure can differ significantly, requiring tailored approaches to meet unique operational and compliance requirements. Small businesses may adopt simplified frameworks, while large enterprises rely on advanced systems to handle complex asset portfolios.

Best practices in asset classification include leveraging established frameworks and standards to promote transparency and consistency. Leading organizations reference global standards such as the MSCI PACS™ asset classification framework to reduce errors and improve reporting accuracy. Common challenges include misclassifying assets, overlooking depreciation or amortization schedules, and failing to update records as asset portfolios evolve. Regular reviews, staff training, and technology integration are essential for maintaining effective asset classification processes.

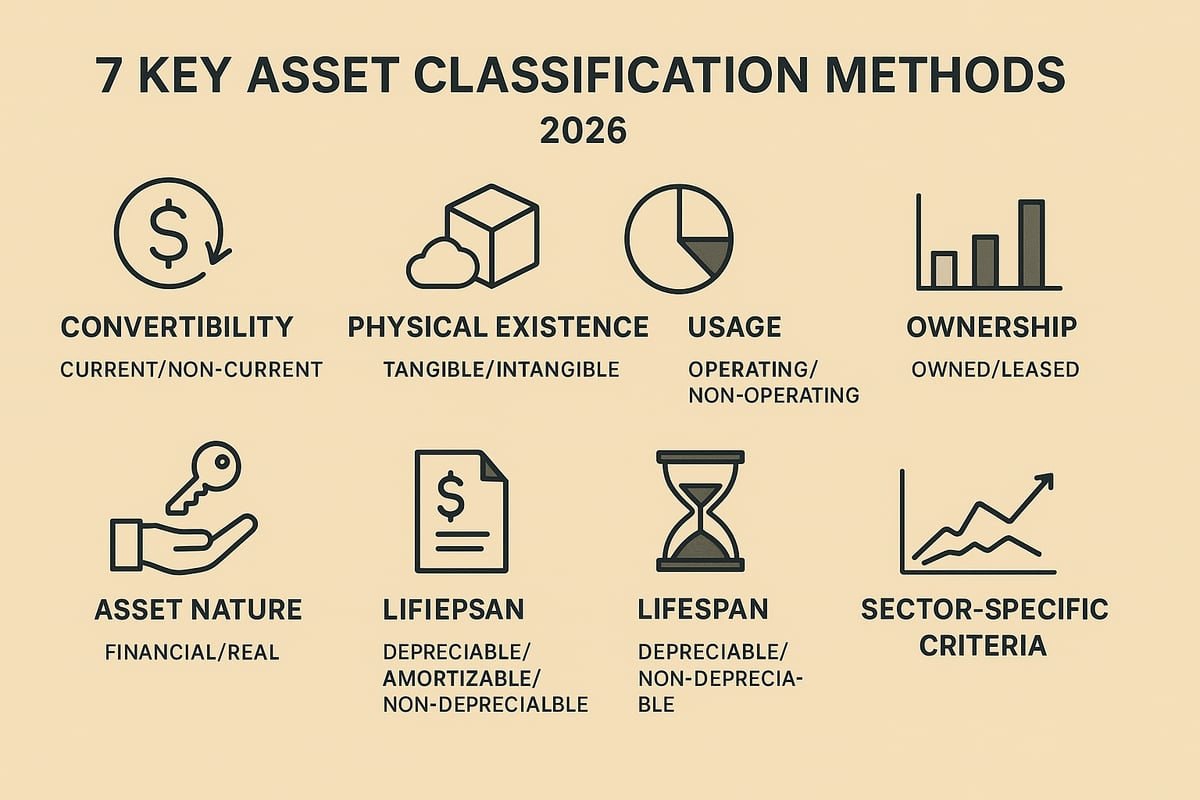

7 Key Asset Classification Methods You Should Know in 2026

Navigating the evolving landscape of asset classification is fundamental for finance, business, and investment professionals in 2026. Understanding these seven key methods empowers organizations to optimize decision-making, manage risk, and ensure compliance. Let’s explore each method, its principles, and real-world impact.

1. Classification by Convertibility (Current vs. Non-Current Assets)

Convertibility addresses how quickly an asset can be transformed into cash, making it central to asset classification. Current assets are those expected to be liquidated within a year, supporting day-to-day operations and short-term obligations. Examples include:

- Cash and cash equivalents

- Accounts receivable

- Inventory

Non-current assets, in contrast, are held for more than one year and play a vital role in long-term strategy. These include:

- Property, plant, and equipment (PPE)

- Long-term investments

- Intangible assets with extended lives

The distinction between current and non-current assets directly impacts liquidity ratios such as the current ratio and quick ratio, which are critical for solvency analysis. For example, a balance sheet clearly separates these categories to help stakeholders assess operational efficiency and risk exposure.

A recent study shows that in the manufacturing industry, current assets typically represent 40 percent of total assets, while in tech, they may be as low as 20 percent, reflecting different liquidity needs. Misclassifying asset convertibility can distort financial ratios and hinder effective asset classification, leading to poor financial decisions.

In summary, mastering convertibility ensures accurate reporting and robust financial health assessments, anchoring the broader asset classification process.

2. Classification by Physical Existence (Tangible vs. Intangible Assets)

Physical existence is a foundational element in asset classification. Tangible assets have a physical form, such as buildings, machinery, vehicles, and furniture. These assets are depreciated over time, reflecting their gradual loss of value.

Intangible assets, meanwhile, lack physical substance but are increasingly valuable in today’s digital economy. Examples include:

- Patents and copyrights

- Trademarks and brand recognition

- Proprietary software

- Goodwill

Intangible assets are typically amortized instead of depreciated. Notably, over 50 percent of the S&P 500’s total value now resides in intangible assets, highlighting their growing significance. For tech firms, intangible assets often dominate balance sheets, while traditional manufacturers may still rely heavily on tangible resources.

Valuing and managing intangible assets presents unique challenges in asset classification. Their worth is often tied to intellectual property rights, competitive advantage, or future cash flow potential. Accurately classifying these assets supports compliance, investment analysis, and strategic planning.

3. Classification by Usage (Operating vs. Non-Operating Assets)

Usage-based asset classification distinguishes between assets essential to core business operations and those that are not. Operating assets are directly involved in daily activities, such as:

- Factory equipment

- Inventory used in production

- Office buildings

Non-operating assets, on the other hand, are not vital to primary business functions. These may include:

- Investment property

- Surplus land

- Marketable securities held for investment rather than operations

This approach to asset classification is instrumental in profitability analysis. Only operating assets contribute to key metrics like return on assets (ROA), while non-operating assets may be candidates for divestment to streamline performance.

For instance, companies often restructure portfolios by selling non-essential assets, freeing up capital for growth or debt reduction. According to leading competitor insights, aligning asset usage with core strategy supports more effective capital allocation solutions and management reporting. This method has helped firms in various industries improve efficiency and focus.

4. Classification by Ownership (Owned vs. Leased Assets)

Ownership is a critical dimension in asset classification. Owned assets grant full legal title and control, such as company-owned buildings, vehicles, and equipment. Leased assets, by contrast, are used under contractual arrangements, with the lessee gaining a right-of-use rather than outright ownership.

Recent accounting standards, including IFRS 16 and ASC 842, have transformed how leased assets are reported. Both types now appear on balance sheets, with leased assets recognized as both an asset and a liability.

The financial implications of this asset classification method are significant. Owned assets are depreciated, while leased assets require amortization of the right-of-use and recognition of lease liabilities. Many organizations have adopted asset-light models, relying more on leasing—especially for technology and fleet management. Post-2024, the leasing of IT and vehicle assets has surged, reflecting new business strategies.

Compliance and reporting challenges persist, particularly when distinguishing between operating and finance leases. Accurate asset classification ensures transparency and supports effective financial decision-making.

5. Classification by Asset Nature (Financial vs. Real Assets)

Asset nature is a core pillar of asset classification. Financial assets include stocks, bonds, and cash equivalents, representing claims on future cash flows or ownership interests. Real assets, in contrast, are tangible resources such as land, buildings, and commodities.

Both types play distinct roles in investment portfolios:

| Asset Type | Examples | Primary Role |

|---|---|---|

| Financial Assets | Stocks, bonds, cash | Liquidity, diversification |

| Real Assets | Land, buildings, gold | Inflation hedge, stability |

Institutional investors, like pension funds, often balance financial and real assets to diversify risk. In recent years, allocations to real assets have increased, driven by the need for inflation protection and stable returns. For example, infrastructure funds and real estate investment trusts (REITs) tailor asset classification to meet sector-specific goals.

The nature of an asset influences its valuation, risk profile, and expected returns. Industry-specific approaches are common, especially in sectors like real estate and commodities, where real assets dominate.

6. Classification by Lifespan (Depreciable, Amortizable, and Non-Depreciable Assets)

Lifespan-based asset classification groups assets by how they lose value over time. Depreciable assets are physical, such as:

- Vehicles

- Machinery

- Office equipment

These assets are systematically depreciated, impacting both tax and accounting records. Amortizable assets are intangible, like patents and trademarks, and are gradually expensed over their useful life.

Non-depreciable assets, such as land, retain their value and are not subject to depreciation or amortization.

Understanding lifespan is crucial for accurate asset classification, as it affects financial statements, tax obligations, and capital budgeting. For example, a company’s capital expenditure plans hinge on the expected depreciation or amortization schedules.

Competitor frameworks recommend automated tracking of asset lifespans to minimize errors and optimize resource allocation. Best practices include regular reviews of asset registers and automated alerts for upcoming depreciation milestones.

7. Classification by Sector or Industry-Specific Criteria

Some industries require tailored asset classification frameworks to meet unique regulatory and operational demands. In healthcare, for instance, asset classification must account for:

- Medical equipment and devices

- Intellectual property (e.g., drug patents)

- Data warehouses supporting compliance and patient care

Manufacturing organizations often track raw materials, work-in-progress (WIP), and finished goods separately to ensure accurate costing and inventory management.

Industry-specific asset classification responds to benchmarks, turnover rates, and regulatory requirements. For example, healthcare organizations increasingly rely on healthcare data warehouse insights to optimize asset tracking and meet compliance standards.

Case studies reveal that companies leveraging sector-specific asset classification achieve higher efficiency, reduced regulatory risk, and better strategic alignment. A tailored approach ensures that assets are managed in line with industry best practices and evolving market needs.

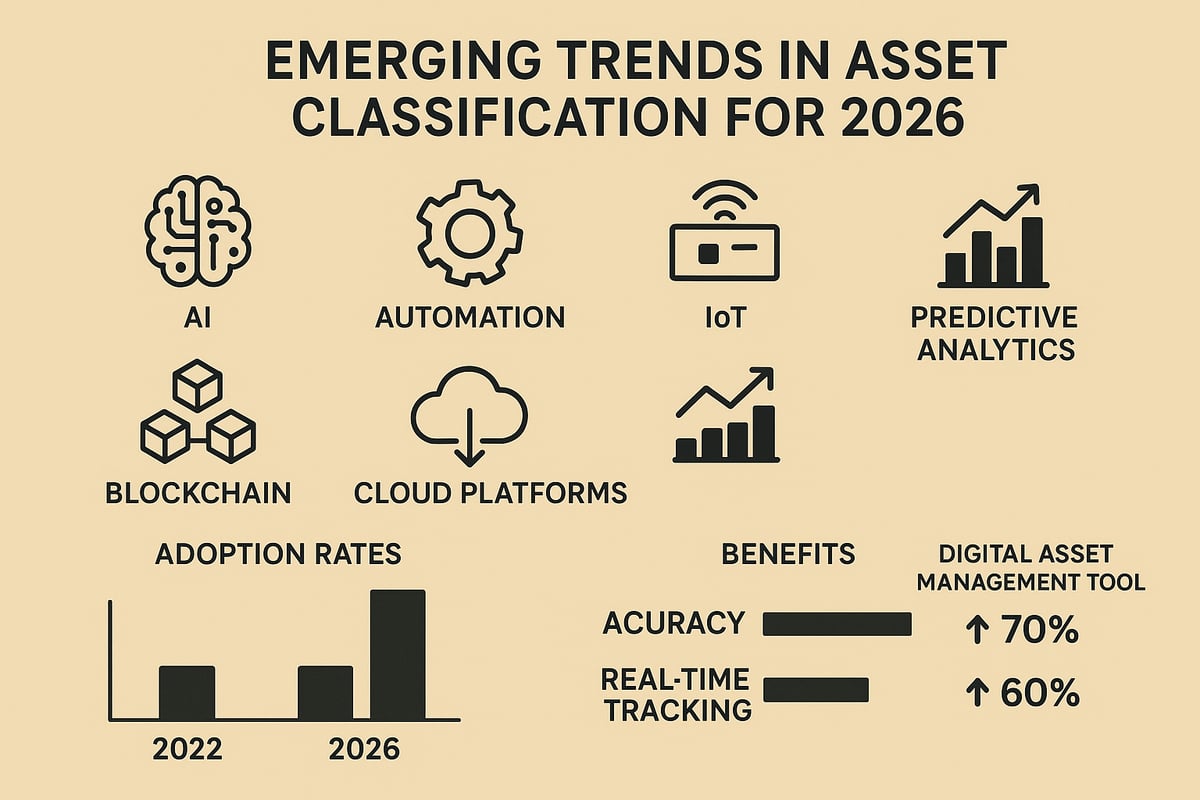

Emerging Trends and Technologies in Asset Classification

The landscape of asset classification is evolving rapidly in 2026. As organizations grapple with growing data volumes and complex asset portfolios, embracing new technologies has become essential. Modern trends are reshaping how companies approach asset classification, making systems more dynamic and responsive.

Artificial intelligence and machine learning are now at the forefront of asset classification strategies. These technologies enable the automation of data sorting, anomaly detection, and predictive analytics, reducing manual workloads and increasing accuracy. Leading organizations are leveraging AI to identify patterns in asset usage and optimize lifecycle management. According to AI’s impact on asset management, firms using AI-driven asset classification report faster decision-making and improved risk controls.

The integration of IoT and blockchain is revolutionizing real-time asset tracking and verification. IoT sensors provide continuous data streams that feed directly into asset classification systems, ensuring up-to-date records. Blockchain adds a layer of transparency and security, making asset histories tamper-proof and auditable. This combination is particularly valuable for industries with high compliance requirements or complex supply chains.

Cloud-based asset management platforms and advanced ERP systems are central to digital transformation in asset classification. These tools offer centralized access, seamless updates, and scalable solutions for growing organizations. As highlighted in Digital transformation in asset servicing, cloud adoption supports dynamic classification frameworks that adapt to regulatory and operational changes in real time.

Recent statistics show that over 60% of global enterprises have implemented digital asset management solutions, with adoption rates expected to climb. Benefits include increased classification accuracy, reduced manual intervention, and real-time reporting capabilities. Organizations that invest in advanced asset classification technologies often experience fewer errors and lower regulatory penalties.

Despite these advancements, challenges remain. Data security, integration complexity, and skills gaps can hinder successful implementation of new asset classification systems. Companies must focus on workforce training, robust cybersecurity measures, and cross-platform compatibility to maximize the value of emerging technologies. Looking ahead, asset classification will continue to evolve, driven by innovation and the need for agility in a fast-paced business environment.

Now that you’ve explored the seven essential asset classification methods for 2026, you know just how much strategic value the right approach brings to compliance, efficiency, and employee empowerment. If you’re ready to cut manual processes, boost your bottom line, and create proactive solutions for your team’s financial and operational health, let’s talk about how you can put these insights into practice. I’d love to help you tailor a strategy that saves time, reduces costs, and positions your organization for success in a fast-evolving landscape.

Book a Consultation